Implied pricing is a real-time valuation derived from the collective probability estimates of traders across a set of prediction market contracts. Rather than waiting for a funding round or an investment bank to publish a number, implied pricing extracts a continuously updated valuation from the spread of prices across binary markets at different thresholds.

On May 26, 2026, Polymarket's implied valuation for Anthropic was $1.0765 trillion. Two days later, Anthropic announced its Series H at $965 billion — Just 11.6% below the market's estimated. This article explains how implied pricing works, why it matters, and where implied pricing exists today.

Key takeaways

What is implied pricing in simple terms?

Implied pricing is a real-time valuation derived from the collective probability estimates of traders across a set of prediction market contracts — not from a funding round, an investment bank, or a company announcement. When traders buy and sell binary contracts on whether a company's valuation will reach specific thresholds, the spread of those prices implies what the market collectively thinks the company is actually worth right now.

How is implied pricing different from an official valuation?

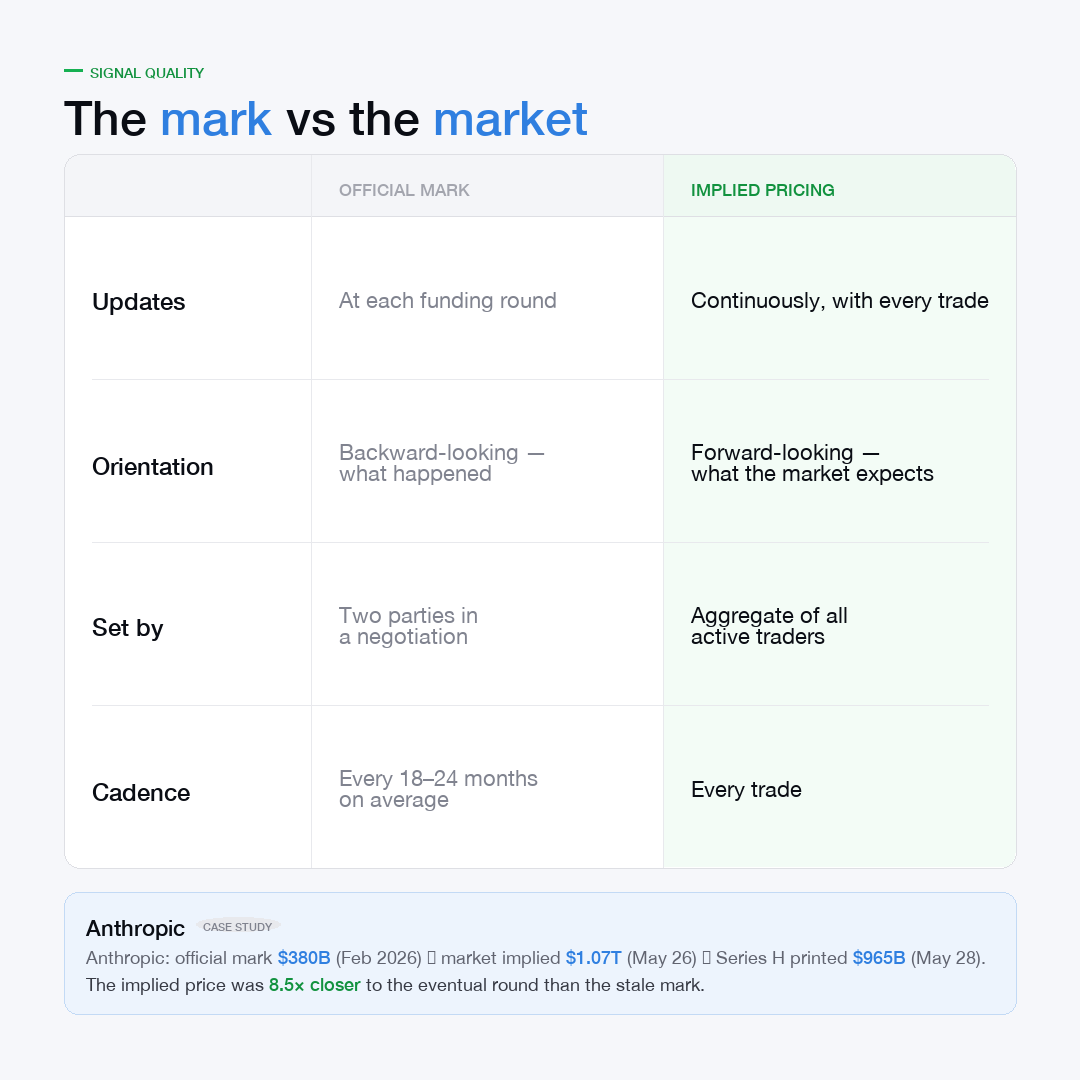

An official valuation is a snapshot — a mark established at a specific moment when two parties agree on a transaction. Implied pricing is continuous. It updates every time a trade is made, in response to every piece of new information, regardless of whether the company has announced anything. Official marks are intermittent by design. Implied prices are not.

How accurate is implied pricing for private companies?

The first real-world test produced a striking result. On May 26, 2026, Polymarket's implied valuation for Anthropic was $1.0765 trillion. Two days later, Anthropic announced its Series H at $965 billion — 11.6% below the market's estimate, but 154% above its previous official mark of $380 billion. The market had captured 84% of the true repricing before the round was announced.

Where can I see implied pricing for private companies?

SOAR runs prediction market ladders on private tech companies including Anthropic, SpaceX, Stripe, and OpenAI. The spread of prices across SOAR's markets produces a continuously updated implied valuation for each company.

The problem with official valuations

Private company valuations have always worked the same way: a company is worth what someone agreed to pay for it, the last time anyone agreed to pay for it. Anthropic's valuation was $380 billion in February 2026. Then, three months later, it was $965 billion. In between, it was officially $380 billion — even as revenues changed, products launched, secondary brokers observed bid formation, and counterparties received fragments of information suggesting the number had moved.

This is not a flaw. It is how private markets were designed. Official marks are established through financing events — funding rounds, tender offers, secondary prints — which happen infrequently by necessity. The median time between funding rounds for high-growth private companies is 18–24 months, per PitchBook. During that gap, the company is repricing continuously in reality. The mark just doesn't reflect it.

Public markets solved this problem decades ago. A trade is the financial expression of a belief about true price. A market — a continuous collection of trades — is the truest form of consensus around the price of an asset. Every second the market is open, it is aggregating everything known about that asset into a single number. Private companies, until recently, had no equivalent.

Is the official valuation ever accurate? At the moment of transaction, yes — it reflects what two informed parties agreed to. The question is how long it stays accurate as the information environment around the company changes. For fast-moving companies in rapidly evolving sectors, the answer is often: not long.

What implied pricing is — and where it comes from

Implied pricing is a valuation derived from the probability prices across a set of binary prediction market contracts on the same company at different valuation thresholds. No single source sets it. No analyst publishes it. It emerges from the aggregate of every trader's judgment, weighted by the capital they're willing to commit.

The mechanism is the same one that makes prediction markets more accurate than polls on well-traded questions. When a trader believes a contract is mispriced — that the market is underestimating the probability that Anthropic's next round prices above $1 trillion — they buy that contract, pushing the price up. When they believe it is overpriced, they sell, pushing it down. The price stabilises where the aggregate of all active traders is roughly balanced. That stabilised price is a probability. And a set of such prices, across a range of thresholds, implies a valuation.

The intellectual foundation runs from Hayek's observation that prices function as information signals — efficiently aggregating dispersed knowledge that no single party possesses — through Robin Hanson's work on idea futures, to the modern prediction market. The point is not that markets are infallible. It is that markets can reward people for revealing information through risk. In private company valuation, where insiders, employees, brokers, and counterparties each hold fragments of the truth but no public channel for what they know, a prediction market gives them one.

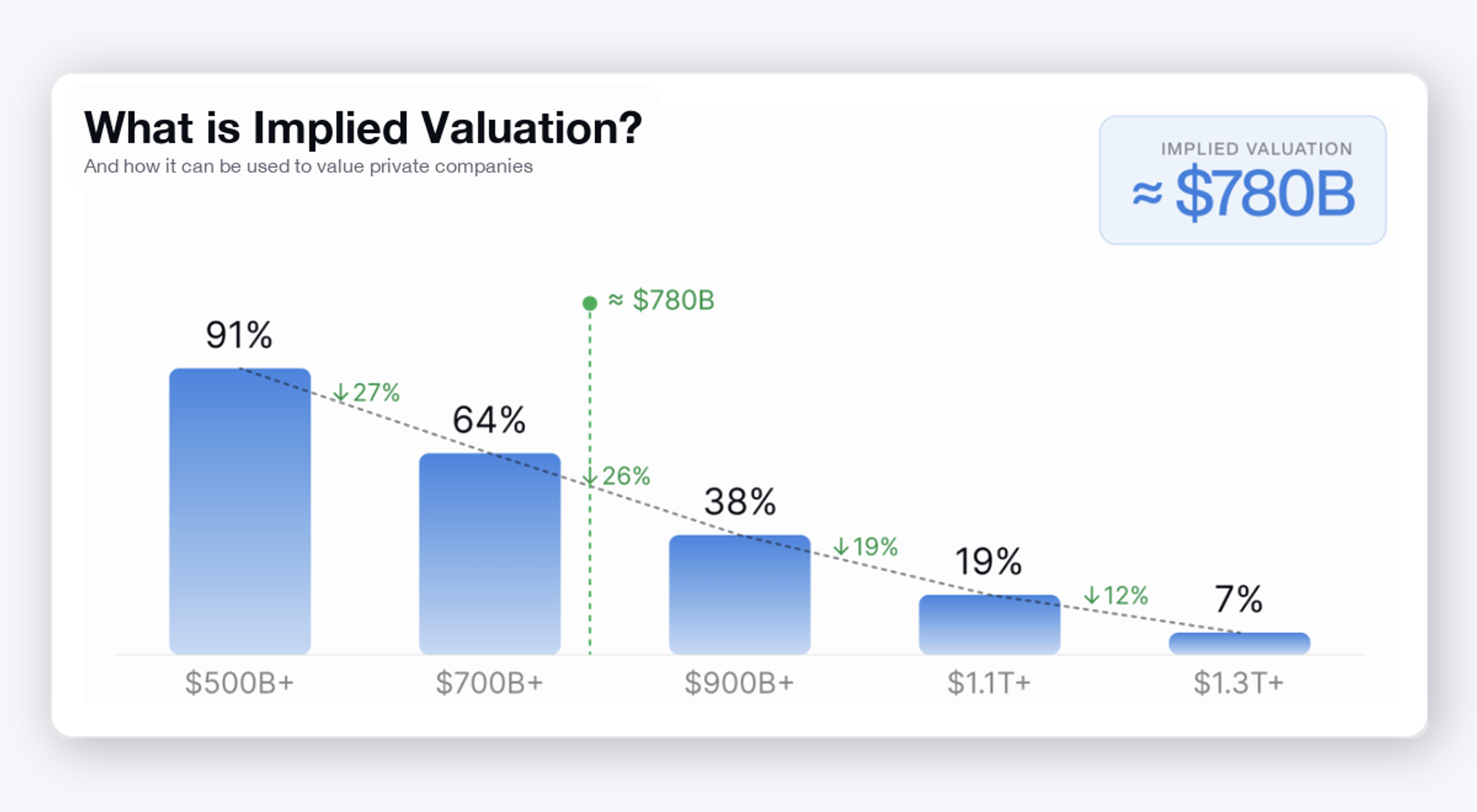

How a valuation ladder works

A single binary contract — "Will Anthropic raise above $1 trillion by June 30?" — yields one probability. A set of contracts at different thresholds yields a curve.

Consider a set of five markets on the same company's next funding round:

- Will the round price above $500B? → 91% yes

- Will the round price above $700B? → 64% yes

- Will the round price above $900B? → 38% yes

- Will the round price above $1.1T? → 19% yes

- Will the round price above $1.3T? → 7% yes

Read from low thresholds to high, these contract prices form a survival curve: the market-implied probability that the company's valuation reaches or exceeds each level. The gap between each contract price represents the probability that the true value falls in that range. The $700B–$900B gap implies a 26% (64% minus 38%) probability that the true value lands between those two thresholds. Aggregate all the gaps and you have a full probability distribution over the company's valuation.

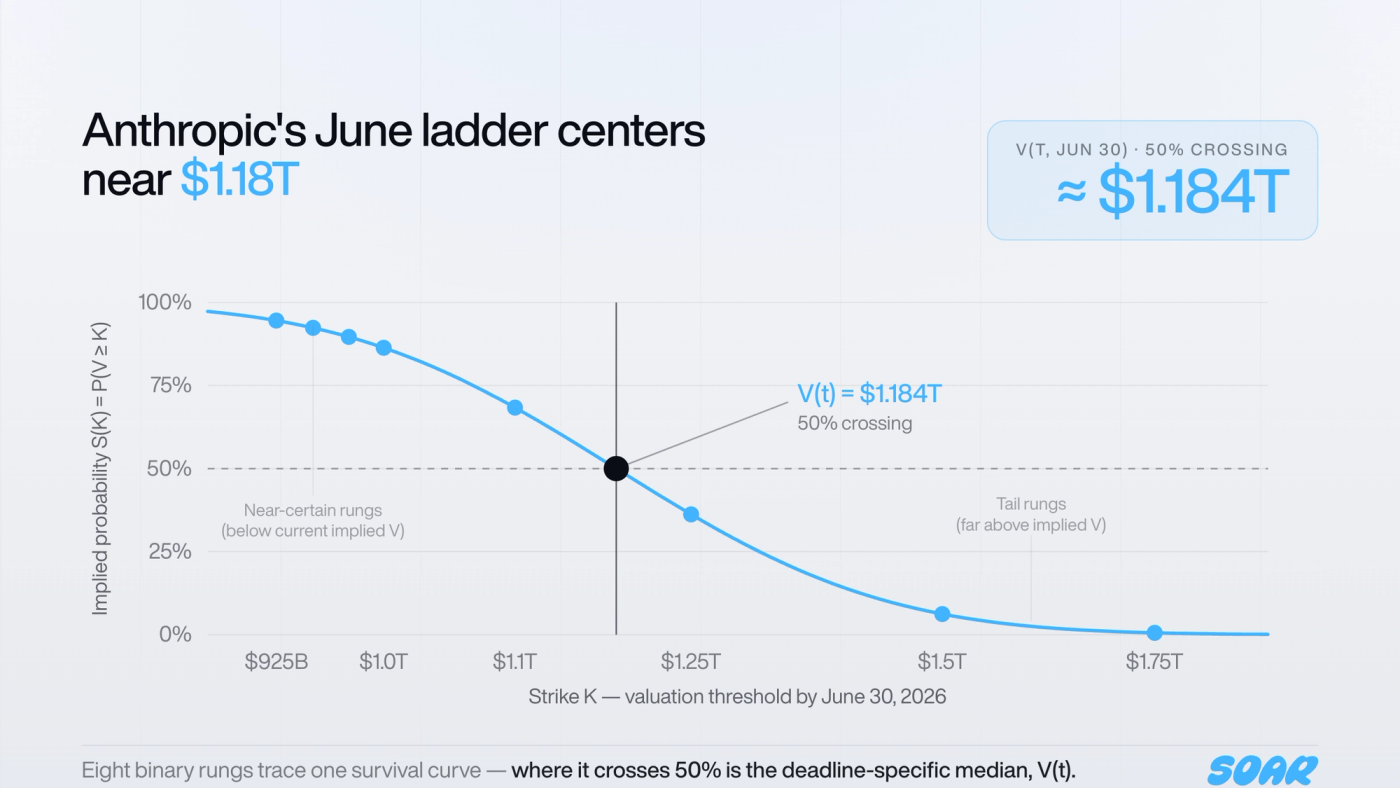

The market-implied median is the point where this curve crosses 50% — the highest threshold at which the market still assigns greater-than-even odds. If the $900B contract trades above 50 cents and the $1.1T contract trades below 50 cents, the median lies between them. Interpolating that crossing gives the ladder's implied valuation.

What is the difference between the median and the spot estimate? The ladder median is a by-deadline estimate — it reflects the probability of reaching a threshold by a specific date, which includes forward-looking time value. The spot estimate, V(t), strips out that time value by fitting a term structure across multiple deadline ladders and reporting the current implied valuation. In the Anthropic case, the June 30 ladder median was $1.1839 trillion, while the term-structure-adjusted spot estimate was $1.0765 trillion. Both are useful; they answer different questions.

The options chain analogy — same logic, different underlying

Implied pricing in prediction markets is not a new idea in finance. Options traders have been doing the same thing for decades — they just call it something different.

When a market maker prices an options chain on a public stock, they produce a set of contracts at different strike prices, each carrying a probability that the stock will be above that strike at expiry. A call option at a $200 strike, trading at $8 on a $180 stock, implies a specific probability that the stock will exceed $200 by expiry. The full chain of strikes — $160, $180, $200, $220, $240 — implies a full probability distribution over the stock's future price. From that distribution, you can back out the market's implied spot price, implied volatility, and the probability mass assigned to any range of outcomes.

The valuation ladder in prediction markets is structurally identical. Each binary contract at a specific threshold is the prediction market equivalent of an options strike. The full ladder of contracts is the prediction market equivalent of an options chain. The implied valuation extracted from the ladder — by finding the 50% crossing of the survival curve and adjusting for time value — is the prediction market equivalent of backing out implied spot from the options chain.

The difference is the underlying. In options markets, the underlying is a publicly traded equity with a continuous price. In prediction market ladders, the underlying is a private company with no public equity — and the contracts resolve against third-party marks like Nasdaq Private Market rather than against an exchange price. That resolution structure introduces differences in timing and precision. But the core logic — aggregating a set of threshold probabilities into a distribution and extracting a point estimate — is the same mechanism options traders have relied on for half a century.

This analogy matters because it grounds implied pricing in established financial practice. This is not a novel or experimental idea. It is a known methodology applied to a new asset class.

Can you calculate implied volatility from a prediction market ladder? In principle, yes — the shape of the probability distribution implied by the ladder encodes information about the market's uncertainty around the central estimate, analogous to implied volatility. In practice, current ladders are too coarse and too illiquid to produce reliable volatility estimates. As ladder granularity and volume increase, this becomes more tractable.

Implied pricing vs the official mark — the Anthropic test

In May 2026, Polymarket launched prediction market ladders on Anthropic and OpenAI — sets of binary contracts resolving against marks published by Nasdaq Private Market. For the first time, a continuously quoted public price existed for private company valuations, with a hard financing event approaching that would allow it to be scored. We create a comprehensive breakdown and statistical analysis of the Anthropic case study, in this article we have a short summary of the findings.

OpenAI — the anchor holds.

OpenAI had completed a primary funding round in March 2026: $122 billion raised at an $852 billion post-money valuation. At the May 26 forecast point, Polymarket's implied valuation for OpenAI was $848.7 billion — a gap of just 0.4% from the March round. The market found no basis for repricing.

Anthropic — the market reprices.

Anthropic's most recent primary round was its Series G, priced at $380 billion in February 2026. At the May 26 forecast point, the implied valuation was $1.0765 trillion — 183% above the official mark. This was not a uniform AI sector movement. OpenAI remained pinned to its March round at the same moment. Anthropic repriced because the information environment had changed: product releases, secondary indications, and rumors of a substantially larger forthcoming financing had reached the market.

On May 28, Anthropic announced its Series H: $65 billion raised at a $965 billion post-money valuation.

The market overestimated by 11.6%. But of the $696.5 billion gap between the stale Series G mark and the market's May 26 estimate, $585 billion — 84% — was confirmed by Series H. The market had repriced the majority of Anthropic's true move before the round was announced.

After the announcement, the implied value declined approximately $35 billion, then recovered above its pre-announcement level. The market treated the official mark as one data point to incorporate — not as a terminal price to adopt. For the first time, part of the repricing between private funding rounds had occurred in public.

Why implied pricing is forward-looking, not just current

The most important distinction between implied pricing and an official mark is not just timing — it is orientation.

An official valuation describes what happened: what parties agreed to, at a specific moment, under specific conditions. It is backward-looking by design.

Implied pricing describes what the market expects to happen. Contracts resolve against future marks, not against the current state of the company. When traders buy a contract on whether Anthropic will price above $1.25 trillion by December 31, they are expressing a view on what the next pricing event will confirm — not just what the company is worth today.

This forward orientation is precisely what makes implied pricing useful for private companies. The information that matters most — the trajectory of the next round, the likelihood of an IPO, the probability of a valuation step-up or step-down — is exactly what prediction market contracts are structured to capture.

The term structure reveals this directly. Different deadline ladders — June 30, December 31 — imply different valuations for the same company at the same moment. The June 30 estimate is higher than the December 31 spot estimate stripped of time value because it incorporates a premium for potential upward movement before that date. That premium is the market's implicit forecast of the trajectory, not just the current level.

Official marks cannot do this. A $380 billion mark is a $380 billion mark until someone decides to update it by raising some funding. Implied pricing updates every time information changes, in the direction of where they think the price should be, just like in the stock market.

Where implied pricing exists today

Implied pricing has existed in public markets for decades — it just hasn't been called that.

Options chains on equities and indices imply a full probability distribution over future price. The full chain of strikes is a ladder. The distribution implied by that ladder is the market's collective forecast of where the index will be at expiry. Backing out the implied spot price, the implied volatility, and the probability mass in any range are all standard operations in options analytics — all relying on the same survival-curve methodology as prediction market valuation ladders.

In crypto, perpetual contracts serve a similar function. A perp trading at a premium to spot implies the market expects spot to move in that direction. The funding rate is itself an implied probability signal about near-term price direction.

Private companies had no equivalent. No options chain, no futures curve, no perp market. The only public signal was the last official mark, potentially years out of date.

Prediction market ladders are the first instrument providing continuous implied pricing for private company valuations. Polymarket launched pre-IPO valuation markets in May 2026. SOAR applies the same mechanic specifically to private tech companies, running continuous ladders on Anthropic, SpaceX, Stripe, OpenAI, and others — not as one-off markets, but as an ongoing price discovery mechanism for companies with no public equity and no options chain.

The methodology is not novel. Options traders have been extracting implied spot prices from strike chains for fifty years. The asset class is. Private companies are for the first time getting the continuous public price discovery that public companies have always had.

The limitations on Implied Pricing you need to know

Implied pricing is not a replacement for fundamental analysis, and it is not infallible.

Liquidity matters — a lot. The Anthropic and OpenAI markets had cumulative volume of approximately $2 million through May 29 — roughly 1,800 times smaller than Polymarket's 2024 US presidential election market. A single large trader can move prices in illiquid markets in ways that don't reflect genuine information. This risk diminishes as volume grows.

The ladder is only as good as its thresholds. If contracts exist at $900B and $1.25T but not at $1.1T, the implied median is interpolated across a $350 billion range. Finer granularity produces tighter estimates.

Implied pricing is forward-looking to a specific deadline. A June 30 implied valuation is a statement about what the market expects will be confirmed by June 30 — not a statement about intrinsic value in perpetuity.

Resolution source risk. Contracts resolving against third-party marks like NPM introduce a dependency on that source's methodology and timing. The mark and the market are answering different questions.

Frequently asked questions

Is implied pricing the same as market cap?

No. Market cap is the share price multiplied by shares outstanding — a direct measure of public equity value based on continuous trading. Implied pricing in prediction markets is derived from probability contracts, not equity trades. It is a market-based forecast of what the next official valuation will be, not a direct ownership claim.

How accurate is implied pricing in prediction markets?

On the first real scored test — the Anthropic Series H in May 2026 — the prediction market estimate was 11.6% above the eventual transaction price, but captured 84% of the move away from the stale prior mark. Polymarket's resolved-market data shows the leading outcome matched final resolution 96.7% of the time four hours before close, and 90.4% one month before close — but those figures apply to high-volume markets, not early-stage ladders.

Can implied pricing be manipulated?

In thin markets, yes. A single large trader can push contract prices in directions that don't reflect genuine information. This risk diminishes as volume grows. In highly liquid markets, manipulation attempts are expensive and typically self-correcting.

Where can I see implied pricing for Anthropic or SpaceX?

SOAR runs continuous prediction market ladders on Anthropic, SpaceX, Stripe, OpenAI, and other private tech companies. The spread of prices across each ladder produces a live implied valuation. Sign up for early access!

How is implied pricing different from a secondary market price?

A secondary market price reflects an actual transaction between a specific buyer and seller. It is a data point, not a continuous market. Implied pricing updates with every trade. Secondary prices are also subject to Right of First Refusal clauses and company approval. Prediction market contracts have no such constraint.

Start trading on SOAR

SOAR is the first platform to apply implied pricing to private tech companies at scale. If you want to take a position on where Anthropic, SpaceX, or Stripe is heading next — without accreditation, without lock-ups, and with flexibility in mind. — SOAR is where that market exists.

Sign up today!

Trading event contracts involves risk and may not be suitable for everyone. You could lose the funds used to enter any transaction. This article is for informational and educational purposes only and does not constitute investment, legal, or financial advice.