The first public valuation test for private companies.

Private markets have a problem.

A company is worth something yesterday, today, and tomorrow, not just when a financing event is announced. The idea that a company is only given a value when a few parties sit around a table exchanging documents is antiquated.

In reality, there is a repricing every second of the day.

Revenues change. New competitors arise. Customers renew or leave. There are changes in marketing, hiring, secondary sales, and everything in between that collectively contribute to the company's value.

Investors, employees, and counterparties may see fragments to suggest a repricing while the official mark is still unchanged. Eventually, you see a press release and a funding round once all is said and done.

Now it's no secret that public markets are the most effective pricing vehicle - whether it's stocks, commodities, currencies, or even collectibles. A trade is the financial expression of a person's belief of what the true price of an asset is, and a market, a collection of trades, is the truest form of consensus around the price of an asset.

Private companies, naturally, have never had the equivalent. They have official milestones: funding rounds, tender offers, secondary prints, and eventually an IPO. Take anthropic, one day the company is worth $380 billion. Months later, it is worth $965 billion.

But now, there is a way to price private companies in public markets.

Prediction markets

At their core, they are incentive-driven information-aggregation machines. When useful information is scattered across people who each hold only a fragment, a properly structured market can turn those fragments into a price. The point is not that markets are magic. It is that markets can reward people for revealing information through risk.

The evidence proves this. Polymarket's resolved-market data reports that the leading outcome matched final resolution 96.7% of the time four hours before close and 90.4% of the time one month before close. That does not make every price correct. It means the market is aggregating information, not just odds.

Most prediction-market attention has gone to public spectacles: elections, sports, Fed decisions, and token prices. Some are useful, but the category has been pulled toward entertainment, while far larger financial markets still lack the kind of information aggregation prediction markets were built to provide.

Private-company valuation is a different case. There is no public ticker. The official valuation is intermittent by design. The current state of the company sits with investors, employees, customers, secondary brokers, and counterparties who have heard pieces of the truth but not the whole thing.

That is precisely the domain prediction markets were built for, yet it remains largely underutilized.

In May 2026, Polymarket launched pre-IPO valuation markets for private companies: public, continuously quoted contracts on whether OpenAI and Anthropic would reach specific valuation thresholds by specific dates. Those contracts did not merely create something to bet on. Read together, they created an implied public valuation.

This paper asks whether that implied valuation carried a real price-discovery signal. Researching a valuation-ladder methodology, we extracted data from the OpenAI and Anthropic markets and scored the results against Anthropic’s Series H financing event.

Reading a Valuation Ladder

An understanding of the underlying market structure is necessary before interpreting the results. Polymarket's pre-IPO market utilizes sets of binary contracts. Each contract asks whether a company's valuation will reach a stated threshold by a stated deadline. A contract trading at $0.80 implies an approximately 80% probability that the threshold will be reached.

Contracts resolve against marks published by Nasdaq Private Market (NPM). In practice, a HIGH-side contract resolves affirmatively if NPM publishes a mark above the stated threshold during the contract window. A LOW-side contract resolves affirmatively if NPM publishes a mark below the stated threshold during the same window.

A single contract yields one probability. A ladder yields a curve.

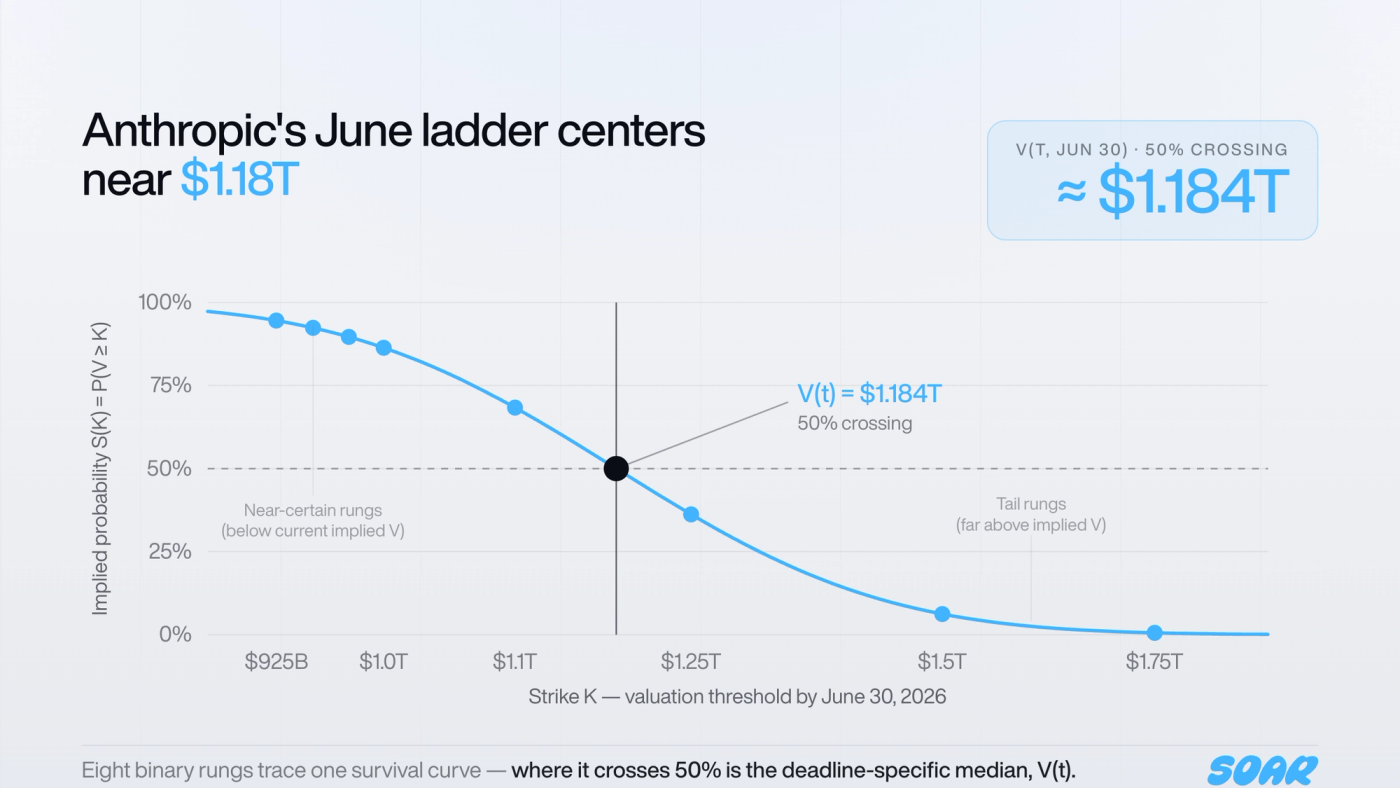

Consider Anthropic's June 30 ladder, which spans thresholds from $750 billion to $1.75 trillion. Read from low thresholds to high thresholds, these contract prices form a survival curve: the market-implied probability that Anthropic's valuation reaches or exceeds each level by June 30. The market-implied median valuation is defined as the point at which this curve crosses the 50% probability level.

The ladder can be understood as identifying the highest valuation threshold at which the market still assigns greater-than-even odds. If the $1.1 trillion contract trades above $0.50 and the $1.25 trillion contract trades below $0.50, the median lies between them. Interpolating this crossing produces the ladder's deadline-specific median estimate.

Each point represents a binary contract at a stated valuation threshold. The curve represents the implied survival function. The 50% crossing yields the deadline-specific median. The spot estimate is lower than the June 30 median because the term-structure fit removes forward-embedded growth.

This median does not yet constitute the model's spot valuation, V(t). Both the June 30 and December 31 contracts contain forward-looking time value. The model therefore fits a term structure across available deadlines and reports V(t) as the current implied valuation after removing the forward slope.

For Anthropic on May 26, this procedure produced a spot estimate of V(t) = $1.0765 trillion. The June 30 ladder median was higher at $1.1839 trillion, reflecting the fact that it is a by-deadline estimate rather than a current-spot estimate.

The full extraction procedure is documented in the Appendix.

The First Test

This initial test of prediction-market-based price discovery is informative in part because the subject companies are not obscure. OpenAI and Anthropic are among the most closely watched firms in the technology sector. Investors, employees, customers, secondary brokers, and competitors each hold fragments of valuation-relevant information. A prediction market provides a venue in which those fragments can surface through prices. The larger the volume of information reaching the market, the more meaningful the resulting valuation estimate.

OpenAI completed a primary funding round in March 2026. In the absence of materially new information, it would be reasonable to expect the market to remain anchored to that transaction. Anthropic presented a different case. Its most recent primary round was older, and the market was processing a sustained flow of product releases, secondary indications, and rumors of a substantially larger forthcoming financing.

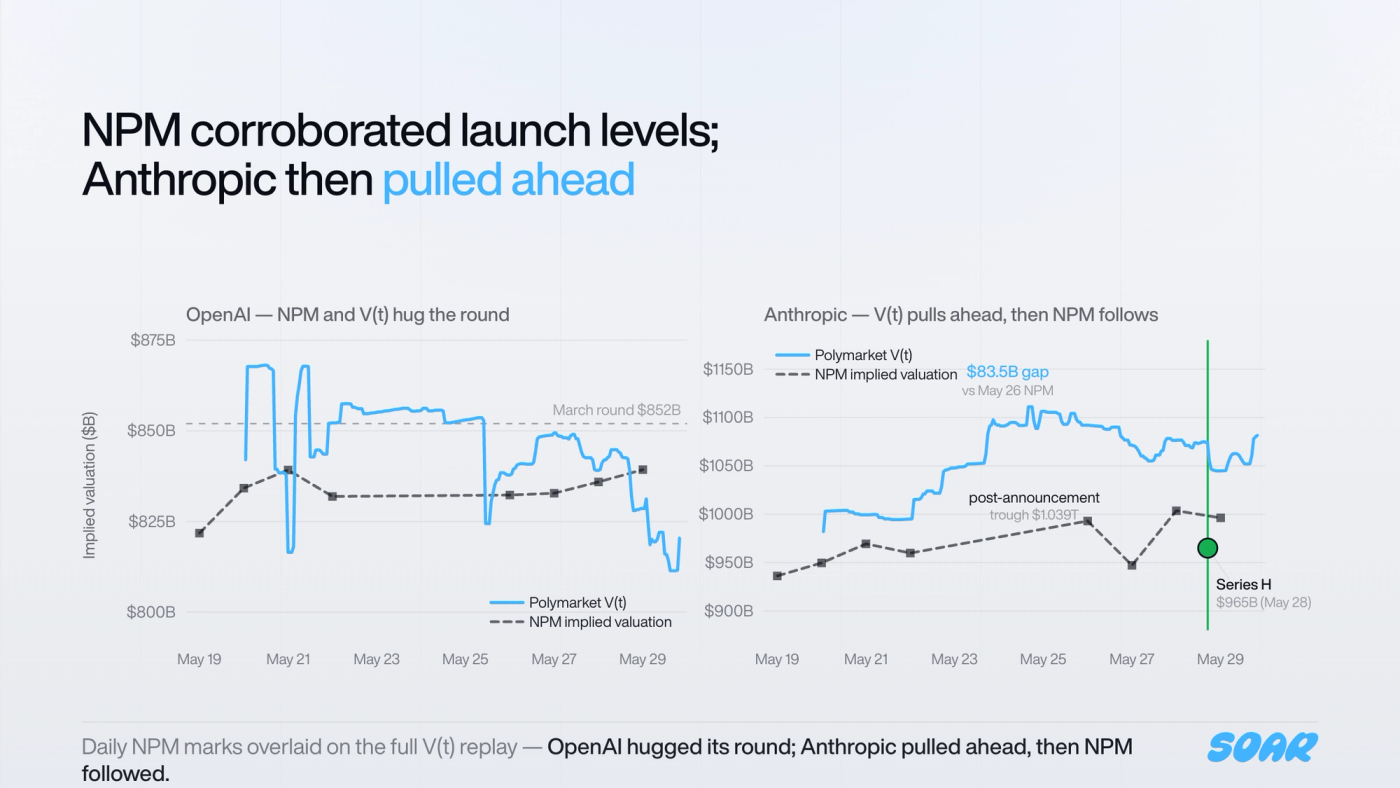

This contrast is analytically important. A market that merely reflected official marks would have kept both companies proximate to their last disclosed rounds. It did not. At the May 26 forecast point, OpenAI remained anchored to its recent transaction, while Anthropic had repriced substantially as participants incorporated available information. Anthropic's Series H was announced two days later, providing a hard valuation event against which the forecast could be scored.

Market-implied valuation indexed to each company's last confirmed primary round. A 1.0x reading indicates the market is positioned at the official mark. The gold line denotes Anthropic's May 28 Series H at $965 billion post-money.

OpenAI: The Anchor Holds

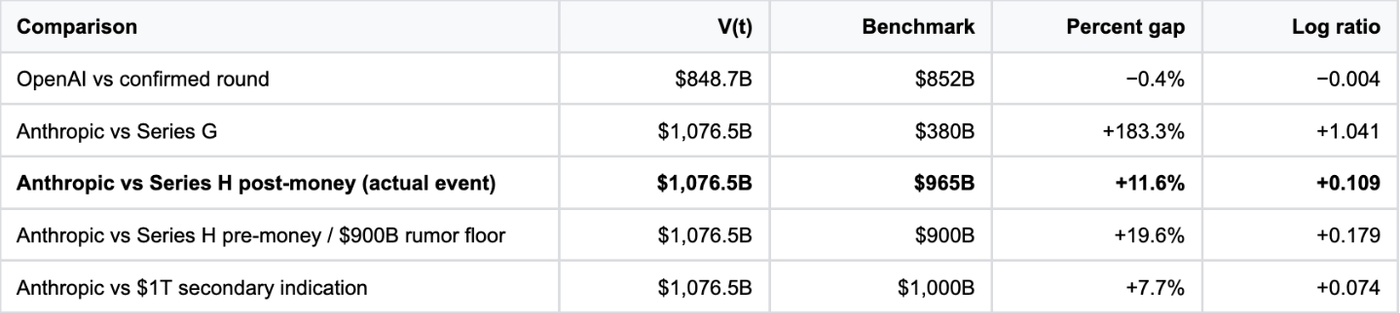

OpenAI announced its most recent funding round on March 31, 2026: $122 billion in committed capital at an $852 billion post-money valuation. At the May 26 forecast point, Polymarket's market-implied valuation for OpenAI was $848.7 billion.

| Benchmark | Value | V(t) | Gap |

|---|---|---|---|

| Primary round, March 2026 | $852B | $848.7B | −0.4% |

Through the May 26 forecast point, OpenAI remained anchored to its March round. Price data alone cannot distinguish whether traders independently arrived at a similar valuation or deferred to the disclosed round in the absence of a stronger countervailing signal. For this analysis, that distinction is less important than the outcome: the market identified no basis for repricing.

OpenAI did drift lower after the forecast point, ending the observation window at $816.0 billion on May 29, representing a 4.2% decline from the March round. This subsequent movement may reflect market repricing following the Anthropic financing announcement, broader sector adjustments, or thin-liquidity effects. It does not alter the scored control result: prior to the Anthropic round's announcement, OpenAI remained within 0.4% of its March transaction.

This result is significant because it demonstrates that the estimator was not mechanically biased toward producing large deviations from prior marks. The same methodology that placed Anthropic far above its stale Series G valuation left OpenAI almost precisely on its March round at the May 26 forecast point. The market was capable of producing a null result, indicating that no repricing was warranted. This property makes the Anthropic departure more difficult to attribute to an artifact of the estimator, the ladder design, or a broad sectoral movement.

Anthropic: The Market Reprices

Anthropic's most recent primary funding round prior to the observation window was its Series G, announced February 12, 2026, at a $380 billion post-money valuation. At the May 26 forecast point, Polymarket's market-implied valuation for Anthropic was $1.0765 trillion.

| Benchmark | Value | V(t) | Gap |

|---|---|---|---|

| Series G post-money, Feb 2026 | $380B | $1,076.5B | +183.3% |

| Series H pre-money / rumor floor, May 2026 | ~$900B | $1,076.5B | +19.6% |

| Series H post-money, May 2026 | $965B | $1,076.5B | +11.6% |

| April secondary indication | ~$1,000B | $1,076.5B | +7.7% |

The market was never proximate to the February round. It entered the observation window at $920.9 billion and settled at $1.0765 trillion by May 26. This gap reflects more than a large percentage move. It demonstrates the market separating Anthropic's implied valuation from an official mark that no longer reflected the information environment. Notably, this was not a case of uniform upward repricing across AI companies. At the same forecast point, OpenAI remained close to its recent round. Anthropic repriced because the information environment around Anthropic had changed.

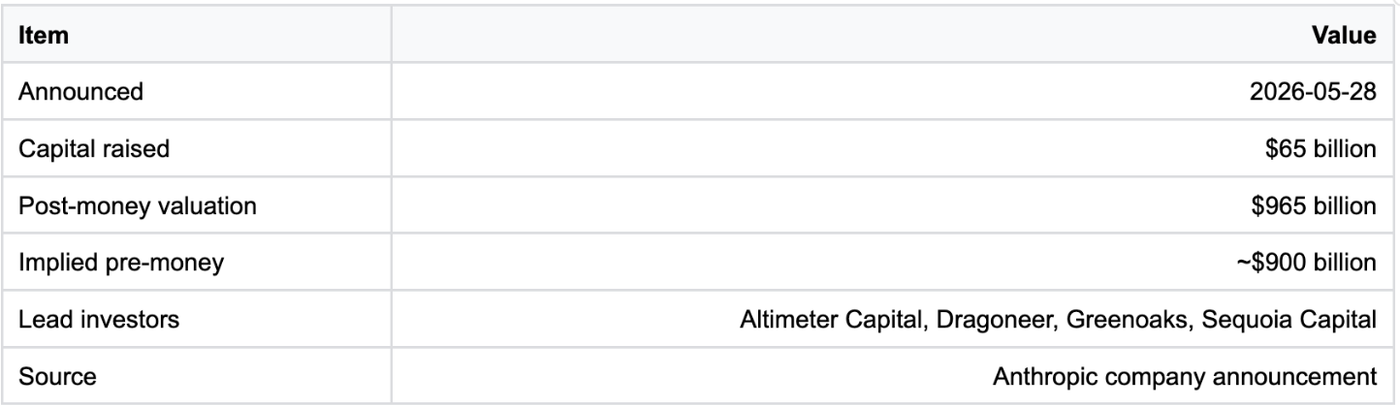

On May 28, Anthropic announced a Series H raising $65 billion at a $965 billion post-money valuation. For the first time, the market's estimate could be scored against a hard private-company valuation event.

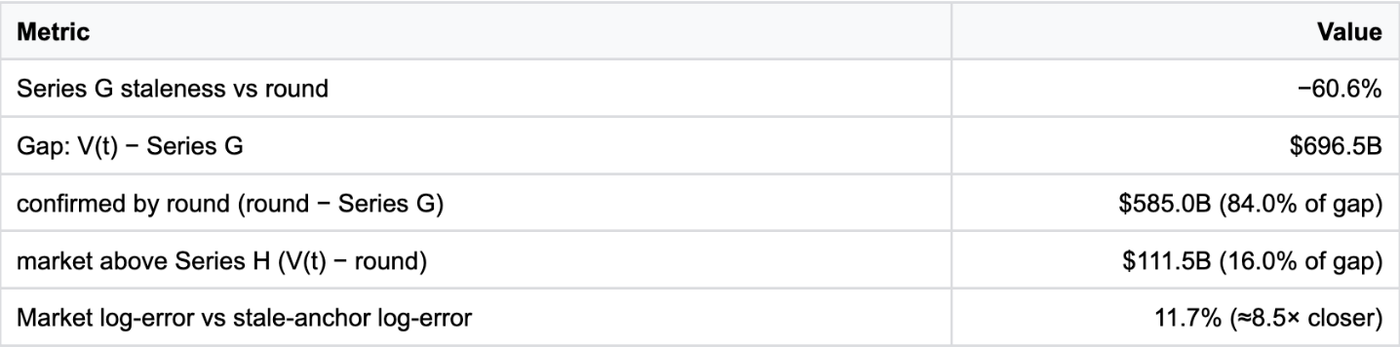

The market did not predict the round with precision. It overestimated the transaction by 11.6%. However, the stale Series G mark underestimated the transaction by 60.6%. Of the $696.5 billion gap between Series G and the market's May 26 estimate, $585.0 billion, or 84.0%, was confirmed by Series H. The remaining $111.5 billion, or 16.0%, represented the market's premium above the eventual round. The estimate was not perfectly precise, but it rendered the prior anchor demonstrably obsolete.

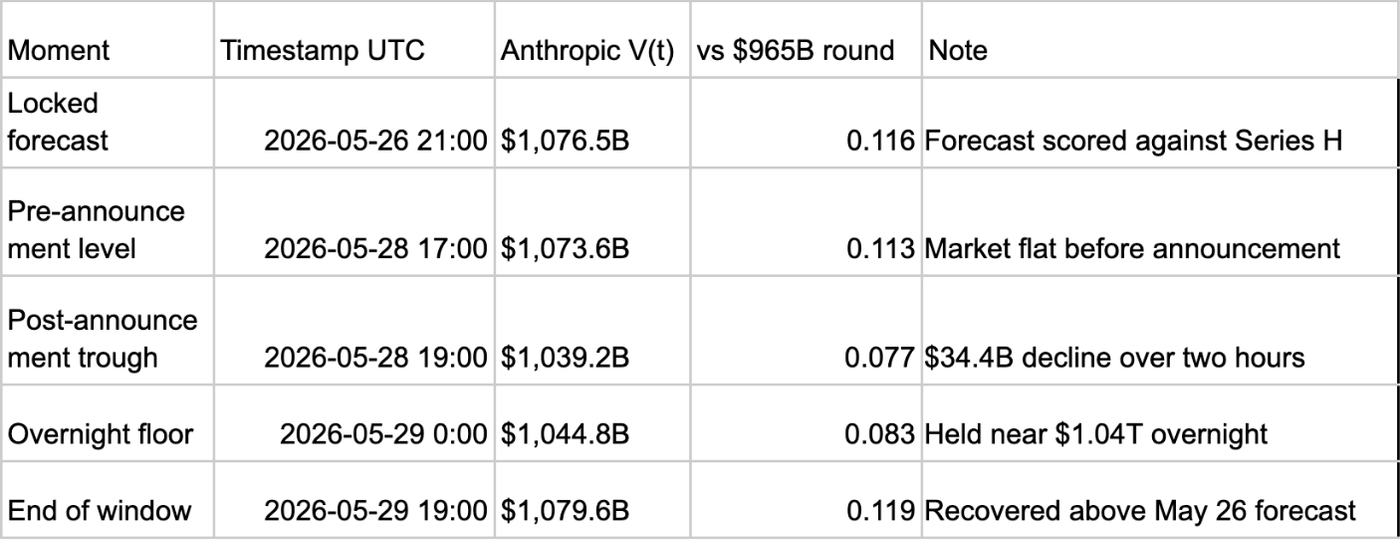

The post-event price path was further revealing. Within hours of the announcement, V(t) declined by approximately $35 billion to an intra-window trough of $1.039 trillion. This decline did not persist. By the following day, the market had recovered, ending the observation window at $1.0796 trillion, slightly above the May 26 estimate and 11.9% above the printed round. The market treated the official mark as a data point rather than a new anchor.

This sequence mirrors the dynamics observed in public equity markets around earnings announcements: a forecast recorded before the event, a hard valuation event, an immediate reaction, and a measurable recovery. The estimate existed before the round, moved when the round was disclosed, and could be evaluated against it, including the market's subsequent decision about whether to converge on the round or return to its prior level.

Gray bars represent public or rumored benchmarks. Gold denotes the Series H post-money valuation. Blue bars indicate Polymarket's May 26 spot estimate and the June 30 ladder median.

NPM: The Mark and the Market

Nasdaq Private Market is not merely a comparison benchmark. It is the contractual resolution source. Polymarket contracts ask whether NPM will report a valuation above each stated threshold by the deadline. This creates a structurally unusual relationship. NPM is a periodic mark constructed from private-market pricing inputs. The prediction market is a forward-looking assessment of where that mark will settle. One functions as the scoreboard; the other provides a continuous feed on the scoreboard's expected future state.

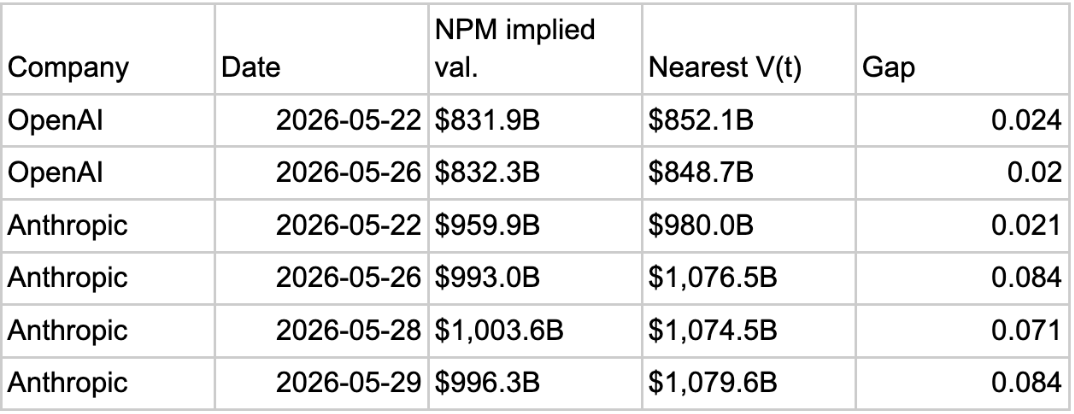

During the initial days of overlap, the two series produced similar estimates. They subsequently diverged for Anthropic. By May 26, NPM marked Anthropic at $993.0 billion while Polymarket's estimate stood at $1.0765 trillion.

NPM was closer to the eventual Series H print. However, NPM is a mark; Polymarket is a market.

Polymarket V(t) and NPM marks tracked closely at launch. Anthropic then diverged upward prior to Series H; NPM re-rated following the round, while Polymarket remained above the Friday mark. OpenAI's late-window decline occurs after the May 26 control point; the scored OpenAI comparison remains the May 26 forecast against the March round.

The NPM comparison raises an important question: to what extent did the market move away from stale public information, and how much of that movement was subsequently confirmed? This question must be precisely defined before the next round arrives.

From One Test to a Scoring Framework

The Anthropic event is analytically useful because it can be scored. However, the objective is not to construct a narrative around a single company after the fact. The objective is to define measurements before the next event arrives.

The question "Did the market price this accurately?" is insufficiently precise. It invites narrative interpretation. A more rigorous approach involves measuring two distances.

The first is the anchor residual: the extent to which V(t) has moved from the last confirmed primary round. If the residual is near zero, the market remains anchored to the prior round. If it is large, the market has determined that the prior mark no longer describes the company's valuation accurately.

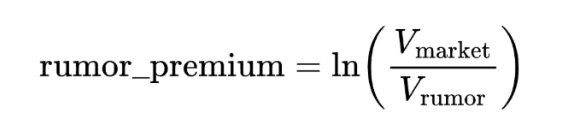

The second is the rumor premium: the extent to which V(t) exceeds or falls short of a reported next-round valuation. This measure separates the component of the market's movement attributable to known rumors from any additional premium assigned beyond the rumored level.

Together, these two measures convert the Anthropic observation from a single case study into a repeatable test. Every future company, NPM mark, secondary print, tender offer, or funding round can be evaluated using the same procedure: compute V(t), record the residuals, await the next hard event, and compare.

These two distances represent the initial, not the final, scoring framework. Additional scoring dimensions will be incorporated as more events resolve.

What These Results Indicate

A single event is insufficient to characterize how these markets will perform across all private companies. It is, however, sufficient to demonstrate that repricing between private funding rounds can become publicly observable before the official mark changes and that the public possesses sufficient information to reprice with some degree of accuracy.

Prior to Series H, the public record indicated that Anthropic was valued at $380 billion. Rumors, secondary indications, and private conversations existed, but no continuously quoted public valuation was available. On May 26, Polymarket implied a valuation of $1.0765 trillion. On May 28, Series H was printed at $965 billion post-money.

For the first time, the pricing between rounds had been done publicly before the round was announced.

Using Series G as the baseline, Polymarket's May 26 estimate was $696.5 billion above it. Series H printed $585.0 billion above it. The new round confirmed 84.0% of the market's movement away from the stale valuation.

The remaining $111.5 billion is where interpretation becomes more complex. Polymarket stood 11.6% above the disclosed Series H mark. Funding rounds are negotiated before they are announced. Polymarket contracts are forward-looking and resolve against future NPM marks, not against the company's press release alone. These markets are also one of the only publicly accessible venues for expressing a tradable view on private-company valuations. When there are few places to take that view, access itself can become part of the price. As a rough private-market benchmark, Notice states that 80% of trades in its database fall within +/-20% of the Notice Price; Polymarket's first scored gap was 11.6%. The market may have been high. It may have been early. It may have been pricing the expected trajectory of the next NPM mark following the round.

The post-event behavior is relevant for the same reason. After the Series H announcement, V(t) declined approximately $35 billion, then recovered to slightly above its May 26 level. The round altered the price, but it did not replace the market's prior assessment. Participants absorbed the announcement and continued to price Anthropic above the disclosed transaction.

That NPM was closer to the Series H print is part of the result and provides comparative discipline. But the Polymarket signal performed a distinct function: it revealed the repricing before the round, the reaction when the round was disclosed, and the premium that persisted after the official figure became public.

The first scored iteration therefore indicates three things. First, the prior $380 billion anchor was obsolete. Second, the majority of the market's departure from that anchor was accurately priced. Third, the component not confirmed by the round did not disappear following the announcement.

The finding is that public price discovery occurred before the private transaction was announced. The market produced an estimate, the round provided a scoring event, and the post-event path revealed how participants updated once the official mark changed.

Limitations

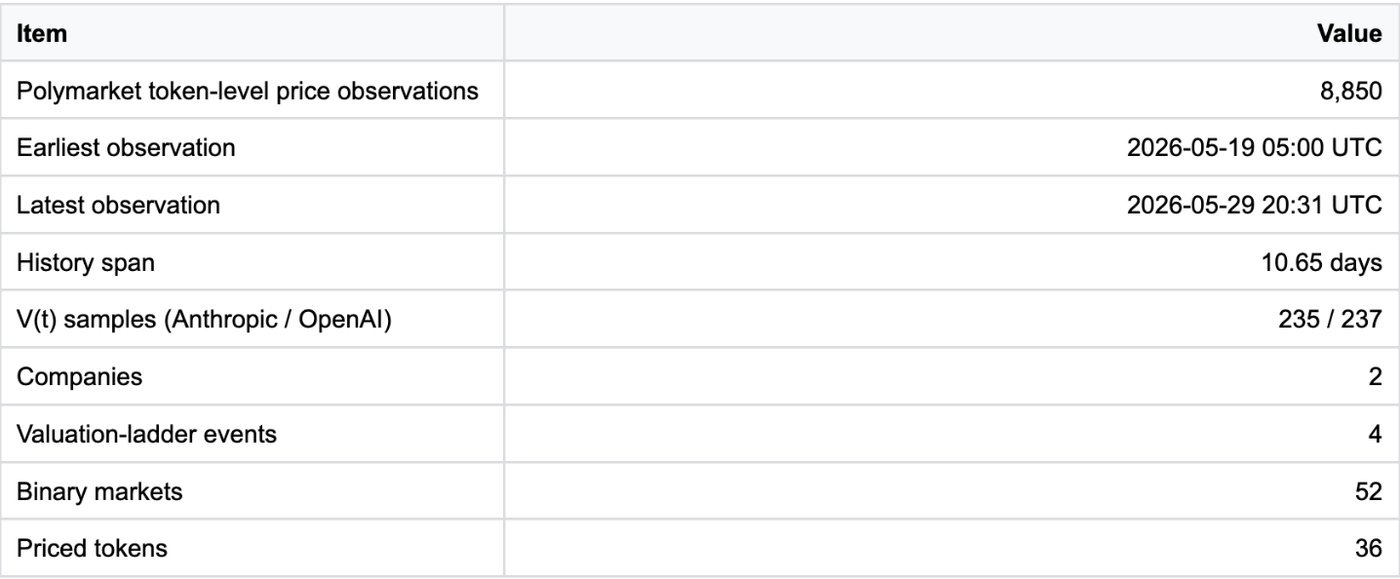

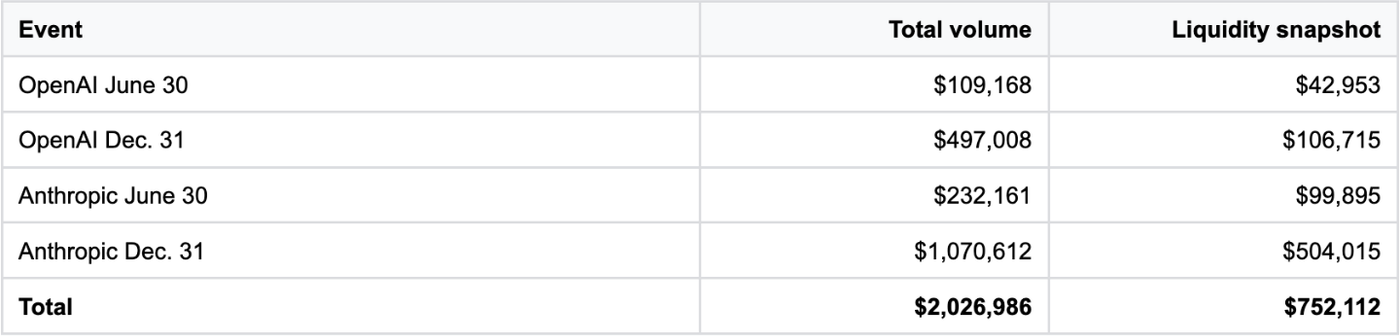

The constraints of this analysis are measurable. The record covers 10.65 days, two companies, four ladder events, 52 binary markets, 8,850 token-level observations, and one hard post-launch financing event. The markets were nascent: cumulative event volume through May 29 was $2.03 million, with $752,112 of resting liquidity. The ladder granularity was coarse — Anthropic's June 30 median was interpolated between the $1.1 trillion and $1.25 trillion thresholds, a $150 billion interval.

This is not the liquidity profile of a mature market. Polymarket's 2024 U.S. presidential election market generated approximately $3.7 billion in volume, roughly 1,800 times larger than the private-company valuation ladders examined here. The post-event recovery may reflect noise, positioning, or genuine forward-looking belief, factors that cannot be fully disentangled at the observed liquidity levels. These are inherent costs of examining a market in its earliest stage. They constrain the generalizability of the results. They do not negate the finding: prior to the Series H announcement, a public market had produced meaningful price discovery away from Anthropic's stale mark.

Conclusion

The observed Anthropic test did not produce a perfect estimate. At the May 26 forecast point, Polymarket implied a value of $1.0765 trillion. Two days later, a Series H was printed at $965 billion post-money. The market priced 11.6% above the disclosed transaction.

Through the Pre-IPO market, the public had repriced Anthropic well before the official valuation changed, effectively pricing in the Series H based on the information that was presented to them. This is consistent with natural price discovery as observed in public markets: information is continuously presented to participants, and prices adjust accordingly based on their beliefs.

It has always been held that markets are the best vehicle for aggregating fragmented beliefs and turning them into a price. In public markets, information is plentiful, and participation is easy and accessible.

Private markets are the opposite case: scattered information, intermittent official mark pricing, and a population of insiders, employees, and brokers with no public channel for what they know.

This first case study, even if modest in scale relative to public markets, was proof that prediction markets can be an effective and accurate vehicle for price discovery of private companies.

Private-company valuations have traditionally been decided by a small group and announced after the fact. In this case, the room still existed, but for once, the price began to leave before the press release did.

Appendix

All figures are pinned to the Polymarket cache as of 2026-05-29 20:31 UTC — the dataset cited in the body. The locked launch-week forecast values reproduce the published numbers exactly. (Additional Polymarket backfill of thin early-window rungs has continued after this cutoff and would produce slightly different historical V(t) values; the version of record is the publication snapshot.)

Data Appendix

Data Scope

Launch-Week Forecast V(t) — Pre-Committed

The forecast scored against the Series H round. Closest replay point at or before 2026-05-26 21:35 UTC.

These round to $849B and $1,077B in the body. The annualized slope is the market-implied term-structure growth rate; it is not a business-growth forecast.

Latest Observation — End of Window

Across May 27–29, Anthropic V(t) reacted to the Series H announcement, then recovered to slightly above the May 26 forecast level (see Real-Time Integration below). OpenAI drifted lower over the same window — a post-forecast-window move that does not affect the scored forecast against its $852B round.

The Series H Event

Forecast Scoring vs the Series H

Forecast V(t) = $1,076.5B (recorded 2026-05-26); round post-money = $965B.

The stale Series G anchor would have been 60.6% below the eventual round; the market's forecast was 11.6% above it. The market's log error (0.109) was 11.7% of the magnitude of the stale anchor's log error (0.932). The market's estimate was roughly 8.5× closer to the eventual round than the stale anchor it replaced.

Real-Time Integration and Recovery — Series H

Hourly V(t) from the morning before the May 28 announcement through the latest observation 26 hours later. The announcement landed around 17:00 UTC.

Key observations:

- No pre-announcement drift. V(t) held flat near $1,073–1,075B through May 28, 14:00–17:00; the market did not anticipate a lower print.

- Reaction window May 28 17:00–19:00. V(t) fell from $1,073.6B (17:00) to a trough of $1,039.2B at 19:00, a $34.4B drop over two hours. Measured against the within-window peak of $1,075.1B (15:00), the max drop was $35.9B, closing about 32% of the forecast's $111.5B above-print gap to the Series H mark.

- Overnight floor May 28 20:00 → May 29 03:00 UTC. V(t) held a tight band around $1,042–1,047B for roughly seven hours.

- Recovery May 29 04:00 → 19:00 UTC. V(t) drifted higher through the morning and afternoon, with a sharp move from $1,049.0B at 16:00 to $1,081.3B at 18:00, settling at $1,079.6B by 19:00.

- Integration unwound. Net effect over the ~26-hour window: V(t) returned to slightly above the May 26 forecast level. The gap to the Series H mark expanded back to $114.6B (+11.9%), essentially matching the forecast's $111.5B (+11.6%) above-print gap. The market reset close to its pre-announcement view rather than converging to the round.

Anchor Residual and Rumor Premium

Forecast values (2026-05-26). Anchor residual = ln(V(t) / V_round); rumor premium = ln(V(t) / V_rumor).

The $900B benchmark was the round's pre-money, so the +0.179 premium confirms the market priced above the rumor, not merely caught up to it. V(t) is a post-money-basis estimate, so the apples-to-apples comparison is against the $965B post-money round (+11.6%).

Polymarket Resolution Mechanics

Each binary contract resolves at the deadline (June 30 or December 31) based on whether Anthropic's or OpenAI's NPM-reported valuation exceeded the contract's stated strike at any point during the contract window. The contract terms designate Nasdaq Private Market as the resolution source, meaning NPM's published valuation marks are the official scoreboard, not Polymarket's own implied V(t).

This has two consequences worth naming:

- The comparison between Polymarket V(t) and NPM is operationally consequential, not just methodologically interesting. NPM's marks determine what the contracts pay; Polymarket's mid-prices reflect what traders believe will happen. When the two diverge — as they did for Anthropic over May 22–28 — the gap is, in some sense, the market betting against NPM.

- The resolution depends on whether the threshold was reached at any point during the window, not just at expiry. This is a one-touch barrier structure: a strike of $1T resolves YES if NPM ever publishes a mark ≥ $1T between contract launch and the deadline, even if NPM is below $1T at expiry. The implied probabilities therefore price first-passage exceedance, not terminal exceedance — a structural difference that raises fair prices relative to a pure terminal-only contract, because every published mark during the window is an opportunity to trigger, not just the expiry mark. The V(t) extracted from the survival curve is correspondingly a first-passage median: the strike at which the market prices even odds of being touched by NPM before the deadline. The effect is largest for rungs near the current valuation and tails off for rungs deep in or out of the money.

NPM Comparison

Figure 4. NPM corroborated launch levels; Anthropic then pulled ahead. Polymarket V(t) sat $83.5B above same-day NPM at the May 26 forecast point; NPM later re-rated to $1,004B on May 28 (Series H announcement day) before settling at $996.3B on May 29.

NPM implied valuations (per-share marks × implied share count), refreshed from the NPM public pricing API through the Friday, May 29 cutoff. NPM publishes trading-day marks at 1:00 PM ET on the following calendar day.

Gap = V(t) relative to NPM. The two independent series tracked within ~3% during the initial overlap window (May 19-22). After May 22, Polymarket V(t) climbed faster than the NPM mark: at the locked May 26 forecast, Anthropic V(t) was $83.5B, or 8.4%, above the same-day NPM.

Around the Series H, NPM printed $1.0036T for May 28 and $996.3B for May 29. Those marks were 4.0% and 3.2% above the $965B Series H print, respectively, while the latest Polymarket V(t) at $1,079.6B remained 8.4% above Friday's NPM mark. The body section reads this not as NPM "winning" or Polymarket "winning," but as the difference between a periodic, gated mark and a continuous, public price.

Market Volume and Liquidity

Cumulative event volume and current resting liquidity, as of 2026-05-29 20:31 UTC.

Launch-week event volume was ~$1.68 million; cumulative volume through the end of the observed window is ~$2.03 million.

Technical Appendix

This appendix records the mathematical specification behind the methodology summarized in the body. The body collapses the math to one paragraph; this section restates it formally and adds implementation details and the event-window accuracy metrics, which the Series H round now instantiates with real values.

Survival Ladder

Each HIGH-side contract pays 1 if the resolved valuation exceeds strike K by the contract deadline. Ignoring fees and microstructure effects, the market mid-price is read as the survival probability:

The HIGH-side ladder is therefore a discrete survival curve across valuation thresholds.

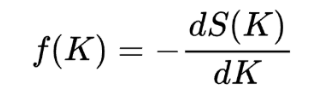

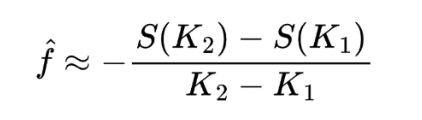

Breeden-Litzenberger Intuition

The implied probability density is the negative derivative of the survival curve:

In the discrete ladder, the density between two adjacent rungs K₁ and K₂ is approximated by:

This is the same family of extraction used to recover implied risk-neutral densities from equity option strips, the same technique, pointed at a new domain. The strikes here are not stock-option strikes; they are private-company valuation thresholds.

Monotonicity

The survival curve should be non-increasing in K: the probability of exceeding $1.25T cannot exceed the probability of exceeding $1T. In practice, quotes can violate this due to stale rungs or thin liquidity. The oracle applies isotonic regression (pool-adjacent-violators) to project observed prices onto a monotone-decreasing curve before extracting any quantile.

Median Extraction

The single central estimate used as V(t) is the strike at which the cleaned survival curve crosses fifty percent:

The implementation interpolates in log valuation space between the two rungs that straddle the 50% crossing. Interpolating in log space is equivalent to assuming the distribution is approximately lognormal, a standard, defensible choice for positive-valued quantities. If the ladder does not straddle 50%, the nearest endpoint is used. This is the V estimate for one ladder at one deadline.

Term Structure

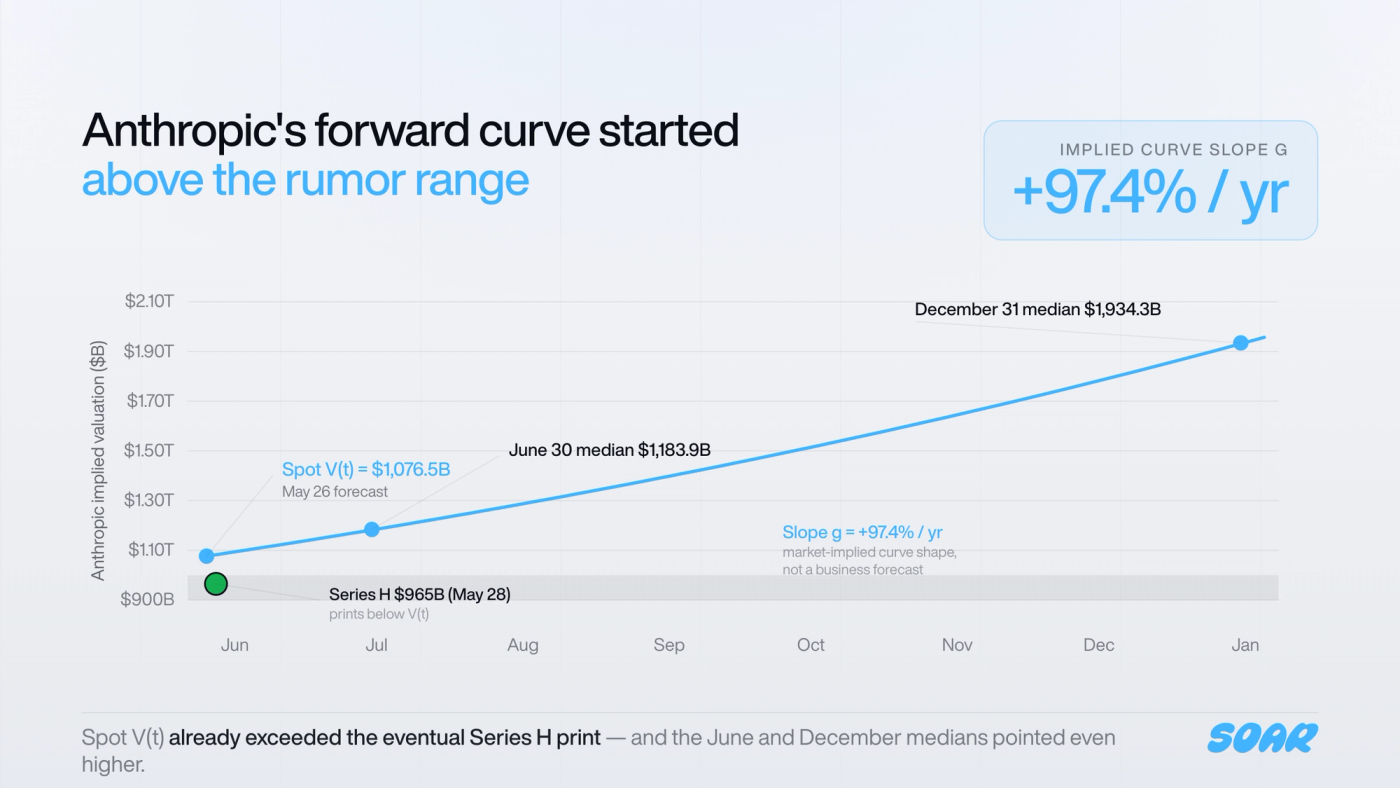

Figure 5. Anthropic's forward curve started above the rumor range. Spot V(t) on May 26 already exceeded the eventual Series H print of $965B; the June 30 and December 31 ladder medians pointed higher still. Slope g = +97.4%/yr is the market-implied curve shape, not a business forecast.

With two ladders at horizons τ₁ (June 30) and τ₂ (December 31), a log-linear term structure is fit across them:

The intercept V_spot is the market's current implied valuation net of time value; the slope g is the daily growth rate embedded in the forward term structure. For Anthropic at the May 26 forecast point, V_spot = $1,076.5B and g = 0.267%/day (97.4% annualized). The $1,076.5B figure, not the $1,183.9B June 30 ladder median, is what the body cites as the market-implied valuation, because it is the estimate for today, not for June 30.

The slope g separates today's spot valuation from forward-embedded optimism; it is not a business-growth forecast. In thin, young binary markets, the slope is a market-implied curve shape, not a business plan.

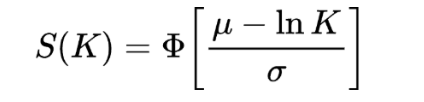

Lognormal Fit (Implied Uncertainty)

If the valuation distribution is approximated as lognormal with parameters μ and σ, then:

where Φ is the standard normal CDF, exp(μ) is the median, and σ is implied log-volatility. σ is estimated via OLS in probit space (drop saturated rungs p ≤ 0.02 or p ≥ 0.98; require ≥3 interior rungs).

Launch-week σ:

The near-term uncertainty is almost identical for both companies (~15% log-vol). The market is not saying Anthropic is harder to price; it is saying both distributions are comparably wide, centered at very different levels. Uncertainty expands to ~47–48% log-vol at the December horizon for both, reflecting genuine fundamental uncertainty about where either company will be in seven months.

Anchor Residual

Zero when the market sits exactly on the last round; positive above; negative below. Using log ratios rather than percentage gaps matters: log ratios are sign-symmetric and composable across time periods. A market doubling from a stale mark and then halving back has offsetting log moves; percentage moves do not behave as cleanly.

Rumor Premium

Rumor benchmarks are not closed transactions, so the measure is range-sensitive. For Anthropic, the relevant range was $900B–$1T; the body reports the premium against both.

Estimator Used

The body and tables use the existing oracle kernel's median estimator on HIGH-side Polymarket ladders without modification. sigma_construction does not affect the median crossing. LOW-side markets are not included in V(t) extraction. Historical values come from replaying token-level price history through the kernel, not from one-shot snapshots at a later wall-clock time.

This version uses HIGH-side ladders only for V(t) extraction. LOW-side rungs are not discarded because they are uninformative; they are excluded to keep the first estimator simple and avoid mixing payoff directions in a thin, young market. A fuller estimator could jointly fit HIGH- and LOW-side rungs, using the LOW-side contracts to constrain the lower tail and improve implied-uncertainty estimation. Whether that tightens or widens σ is empirical: in clean liquid markets, it should improve identification, but in thin markets it may also reveal inconsistency or noise.

Why the Median Estimator?

Five estimators were evaluated in prior research: median, Breeden-Litzenberger risk-neutral mean (rn_mean), trimmed multi-quantile, lognormal MLE, and a geometric ensemble. A sixth — a 1D extended Kalman filter on ln V — was added later.

The binding constraint for selection is reflexive stability: in a self-resolving market whose market makers revert toward a published V̄, any estimator with a bias at the fair-priced fixed point self-amplifies. Empirically, in a no-change stability test, the risk-neutral mean drifted +313% and the geometric ensemble +93% over 30 days; the median, trimmed multi-quantile, lognormal MLE, and Kalman estimators were unbiased and stable.

Among the stable four, the median is chosen for v1 because it is:

- The simplest implementation — find the strike where the cleaned survival curve crosses 50%, log-linear interpolation between the straddling rungs.

- The most robust to thin and saturated rungs — a clipped 99¢ rung doesn't move the median crossing, whereas it inflates the risk-neutral mean integral and shifts the lognormal MLE fit.

- Insensitive to sigma_construction — the kernel's auxiliary σ parameter does not affect the median's output, so it doesn't introduce a tunable knob that would need to be calibrated against live data.

- Empirically close to the lognormal MLE in dense, well-quoted regimes within ~3× of MLE on simulated single-strike attack costs.

The Kalman filter is the natural upgrade path for sparse books (Tier-3 names, cold starts) because it provides a free posterior-variance signal usable as an uncertainty band. For dense Tier-1 markets like OpenAI and Anthropic at v1, the median is sufficient and legible.

Source Notes

- Robin Hanson, "Futarchy: Vote Values, But Bet Beliefs": https://mason.gmu.edu/~rhanson/futarchy.html

- University of Iowa Tippie timeline on the Iowa Electronic Markets, founded in 1988: https://tippie.uiowa.edu/about/who-we-are/tippie-timeline

- Breeden and Litzenberger, "Prices of State-Contingent Claims Implicit in Option Prices," Journal of Business, 1978: https://ideas.repec.org/a/ucp/jnlbus/v51y1978i4p621-51.html

- OpenAI March 31, 2026 financing announcement: https://openai.com/index/accelerating-the-next-phase-ai/

- Anthropic Series G announcement, Feb. 12, 2026: https://www.anthropic.com/news/anthropic-raises-30-billion-series-g-funding-380-billion-post-money-valuation

- Anthropic Series H announcement, May 28, 2026: https://www.anthropic.com/news/series-h

- TechCrunch on Anthropic's reported $850B–$900B preemptive offers: https://techcrunch.com/2026/04/29/sources-anthropic-could-raise-a-new-50b-round-at-a-valuation-of-900b/

- TechCrunch on Anthropic's Series H: https://techcrunch.com/2026/05/28/anthropic-raises-65-billion-nears-1t-valuation-ahead-of-ipo/

- Polymarket Privates live market page: https://polymarket.com/predictions/privates

- Nasdaq Private Market publisher page: https://data.nasdaq.com/publishers/NPM

- Polymarket, “How accurate is Polymarket?”, accessed June 2, 2026, https://polymarket.com/accuracy/

Methodology: median estimator on HIGH-side valuation ladders via existing oracle kernel; term structure fitted log-linearly across June 30 and December 31 horizons. Launch-week forecast (V(t) = $1,076.5B) recorded 2026-05-26; the Series H round ($965B post-money) announced 2026-05-28; post-announcement integration and recovery measured from hourly V(t) through 2026-05-29 19:00 UTC. Cache snapshot pinned at 2026-05-29 20:31 UTC for this version of record.