What Are Synthetic Assets? (And How They Apply to Private Company Investing)

Introduction

If you've ever traded an S&P 500 future, bought a gold ETF, or held a CFD on Tesla stock, you've used a synthetic asset. The concept is older than the term — futures contracts have existed since the 1800s — and over the past two decades, markets have built increasingly sophisticated ways to engineer exposure to anything that has a price.

The most interesting application is also the newest. Private companies like Anthropic, SpaceX, and Stripe represent more than $10 trillion in combined value, and almost nobody can directly own a piece of them. For the first time, synthetic instruments are quietly making that exposure available to ordinary investors — and the rest of this article is about how that's happening.

Key takeaways

What is a synthetic asset?

A synthetic asset is any financial instrument that replicates the economic exposure of another asset without requiring direct ownership. Common examples include futures contracts, CFDs, synthetic ETFs, tokenized crypto assets, and prediction markets.

Why do synthetic assets exist?

Synthetic instruments solve four access problems: regulatory barriers, capital minimums, illiquidity, and absence of an underlying tradable market.

Can you get synthetic exposure to private companies like Anthropic or SpaceX?

Yes — through prediction markets. Traditional synthetics don't exist for private companies, but platforms like SOAR offer prediction market positions on private company valuations, funding rounds, and IPO timing.

What makes an asset synthetic?

A synthetic asset is engineered exposure to an underlying asset, replicating its price movements, dividends, or returns through a separate contract or instrument without conferring direct ownership.

If you can hold something that goes up and down with Tesla's stock price without ever owning a share of Tesla, you have synthetic exposure. It might be an option, an event contract, a tokenised equity or SPV — but the underlying logic is identical: track the asset, don't own it.

Three properties show up in every synthetic, no matter the wrapper:

• Replication. The instrument tracks the underlying closely enough that holding the synthetic produces roughly the same economic result as holding the real thing.

• No direct ownership. You hold a contract, a token, or a position that references the asset — not the asset itself.

• Two-way exposure. Synthetics let you participate in upside and downside. They're not bets, they're substitutes for ownership.

Synthetics exist for four reasons, and almost every successful one solves at least two: access barriers, cost, efficiency, and regulation. When an underlying is hard to buy directly, expensive to hold, slow to trade, or restricted by who can transact, synthetics fill the gap.

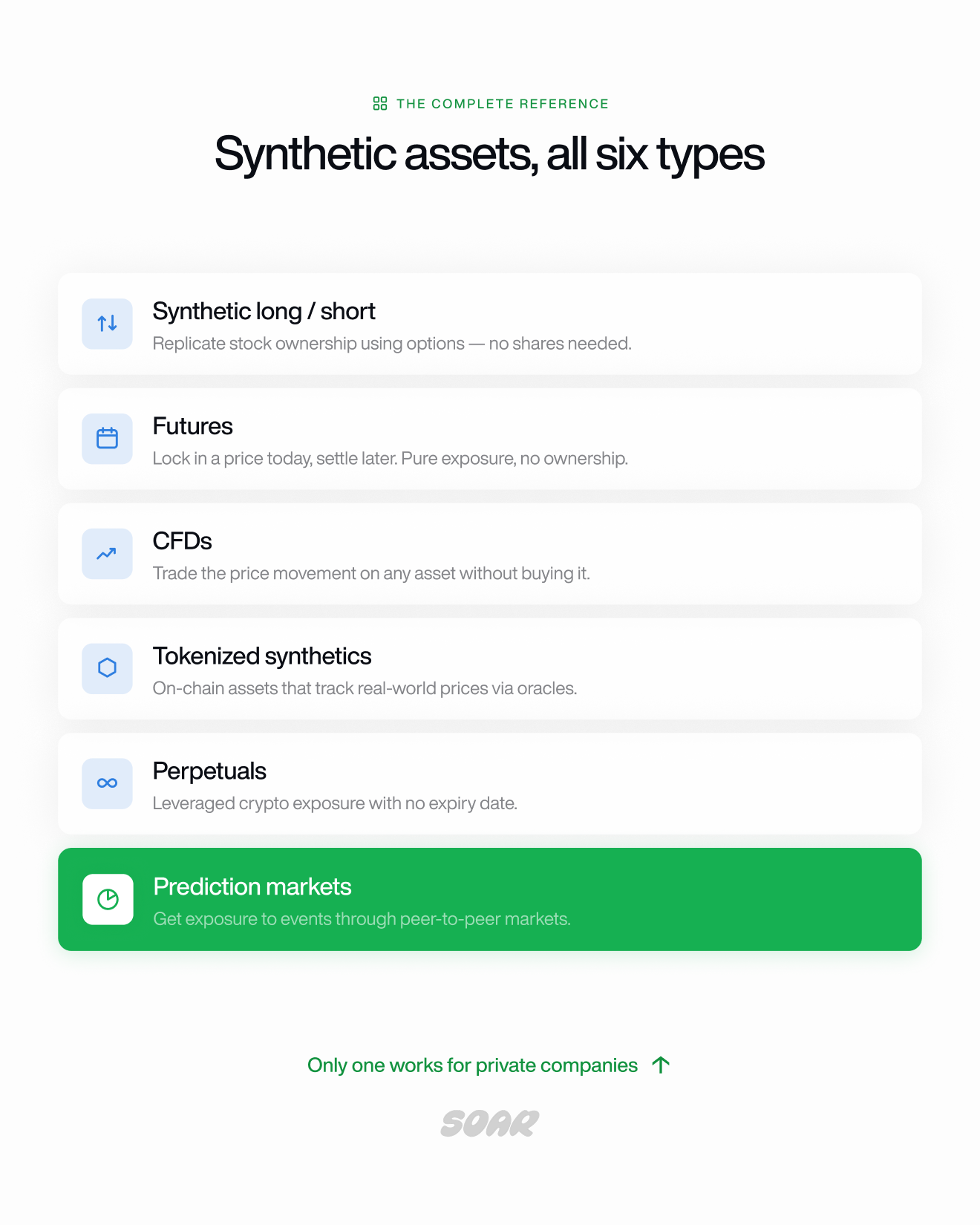

The six synthetic instruments worth knowing

The most widely used synthetic instruments are synthetic long/short positions, futures, CFDs, tokenized synthetics, perpetuals, and prediction markets. Each replicates exposure to an underlying without direct ownership, but they each have their differences.

Synthetic long/short positions (Options)

A synthetic long combines a long call option and a short put option at the same strike and expiry to replicate the economic exposure of owning a stock, without buying the underlying shares. A synthetic short reverses the trade.

This is the textbook example. Options traders use it constantly because the combined position behaves almost identically to owning the stock, but it ties up far less capital. It's not glamorous and it doesn't generate headlines, but it is widely used on wall street and in the upper echelons of finance.

Futures contracts

A futures contract is an exchange-traded agreement to buy or sell an asset at a set price on a future date, giving the holder pure synthetic exposure to that asset's price movement without ever owning it.

Futures are the oldest synthetic and still the largest. The S&P 500 E-mini future alone trades around $300 billion in notional volume per day, according to CME Group, and similar markets exist for oil, gold, currencies, and rates. Most institutional exposure to those markets is synthetic.

CFDs (contracts for difference)

A contract for difference is an agreement between trader and broker to exchange the difference between an asset's opening and closing price, letting the trader take a position on price movement without owning the asset.

CFDs are the dominant retail synthetic in the UK and EU. They're leveraged, easily accessible, and — depending on who you ask — either democratizing or dangerous. The UK Financial Conduct Authority has found that the majority of retail CFD accounts lose money, mostly because the leverage that makes CFDs interesting is also what blows them up. In the United States, CFDs are banned for retail traders entirely.

Tokenized synthetics

Tokenized synthetics are blockchain-based tokens that track the price of real-world assets through oracle price feeds, letting crypto-native users hold synthetic exposure to stocks, commodities, or indices on-chain.

The biggest examples are Pre-Stocks (SPV-backed tokens) and Synthetix (who issue tokens like sTSLA, sBTC, and sGOLD that mirror their underlying assets through smart contracts). The pitch is global accessibility — anyone with a wallet can hold synthetic Tesla without a US brokerage account — and the catch is regulatory ambiguity plus reliance on oracle accuracy.

Perpetual contracts

A perpetual contract, or perp, is a futures contract with no expiry date, settled continuously through a funding rate mechanism that keeps the perp price anchored to the underlying spot price.

Perps were invented in crypto and never left. They're now the dominant leveraged instrument for trading Bitcoin, Ethereum, and now on tokenized equities — daily perp volume on exchanges like Binance, Bybit, and Hyperliquid routinely exceeds $100 billion, per CCData and CoinGecko reporting.

Prediction markets

Prediction markets are contracts where traders buy and sell positions on the probability of a specific outcome, with prices reflecting continuous market consensus on the likelihood of that outcome occurring.

For the last few years, prediction markets meant Polymarket and Kalshi, and they meant elections, sports, and macro. What's interesting now is that prediction markets are being applied to private companies - through platforms like SOAR - where no public underlying asset exists. There's no options market on Anthropic. No futures on SpaceX. No CFDs on Stripe. Prediction markets work because they don't need any of those — they create their own price discovery from market consensus and implied pricing

What is implied pricing in prediction markets?

When you run multiple yes/no markets on the same asset at different price thresholds, you can calculate a single implied valuation from the spread of probabilities.

It's what the market collectively thinks something is worth, updated in real time with every trade.

Other synthetics worth knowing, briefly

Total return swaps, synthetic ETFs, credit default swaps, synthetic CDOs, ADRs, structured notes and warrants — same principle in every case. Engineered exposure without direct ownership. Most live inside institutional portfolios rather than on retail platforms.

Why does synthetic exposure matter for private companies?

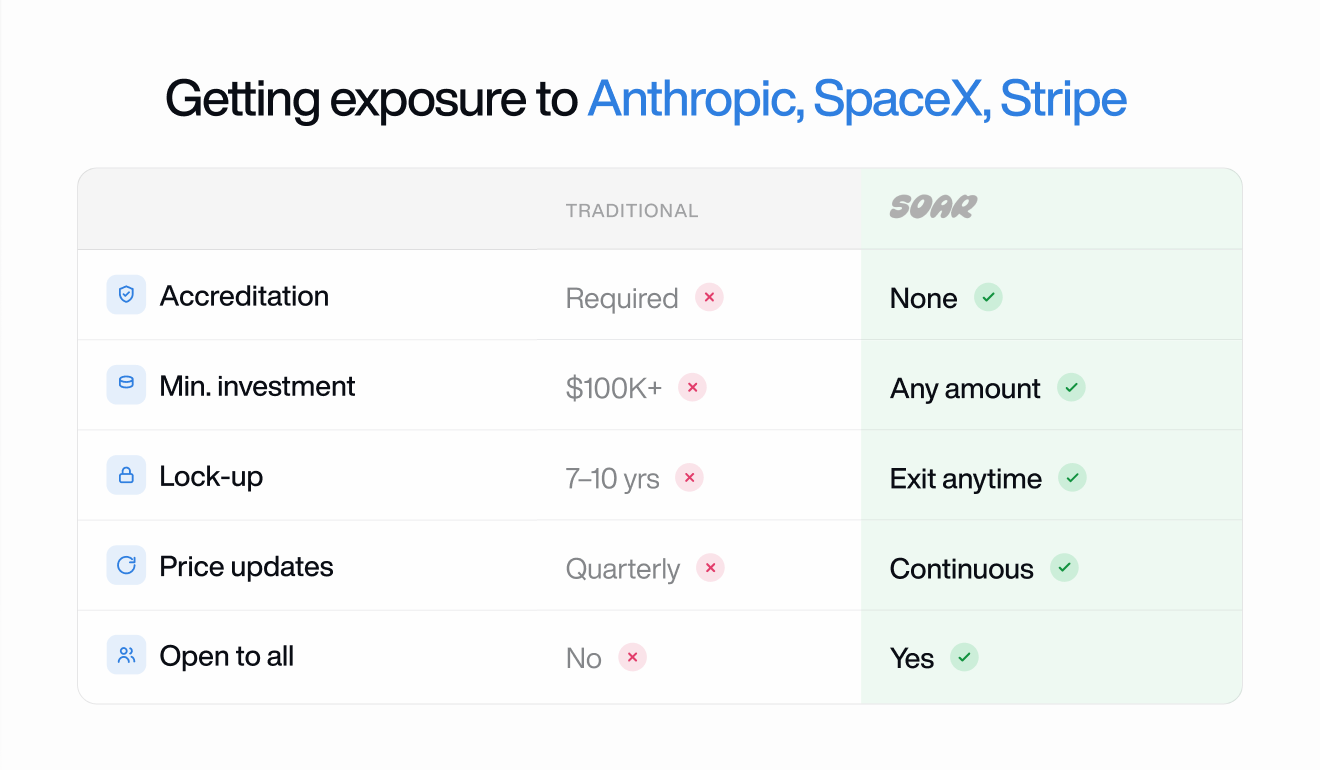

Synthetic exposure matters for private companies because roughly $10 trillion in value sits in companies that almost no retail investor can directly access. Synthetics are the only way to open that door for the everyday investors, but traditional synthetic instruments (options, futures, CFDs) don't exist for them.

The world's most valuable private companies — including SpaceX (reportedly valued at around $350 billion based on secondary market trading data from Hiive and Forge), Anthropic (valued at $965 billion in its May 2026 funding round per company announcements), and Stripe (valued at $91.5 billion in February 2025 according to Bloomberg)— typically stay private for 10 years or more.

Those barriers are stacked:

• Accreditation requirements. SEC Regulation D requires US investors to earn $200,000+ annually (or $300,000 jointly), or hold $1 million+ in assets, to invest directly in most private offerings.

• High minimums. Forge and EquityZen typically require $10,000–$100,000 per investment.

• Lock-up periods. Direct equity investments are illiquid for 7–10 years until an exit event (assuming you got in at the earlier rounds).

• Stale price discovery. Valuations only update when the company raises a new round — often 18–24 months apart. These numbers depend on the speed of a companies growth and vary

• Transfer restrictions. Right of First Refusal clauses and company approval block most secondary transactions.

None of the traditional synthetic instruments work here. There are no listed options on Anthropic. No futures market for SpaceX. No CFDs on Stripe. The instruments that solve access problems in public markets simply don't exist for private ones — which is why prediction markets, the first synthetic instrument that doesn't require an existing tradable underlying, have become the route through.

How does SOAR let you trade private companies?

SOAR is a platform where you can trade private companies. Using the mechanism of prediction markets built specifically for private tech companies, SOAR offers synthetic exposure to Anthropic, SpaceX, Stripe, and a growing roster of others through tradable positions on their valuations, funding outcomes, and IPO timing and more.

The mechanics are straightforward. SOAR runs markets on well-defined outcomes — Will Anthropic raise above a $100 billion valuation in 2026? Will SpaceX IPO before 2027? Will Stripe's next round price above $120 billion?

Each market has continuous pricing driven by what traders collectively think will happen, and positions gain or lose value as that consensus shifts. Implied pricing on private companies can then be derived from these markets.

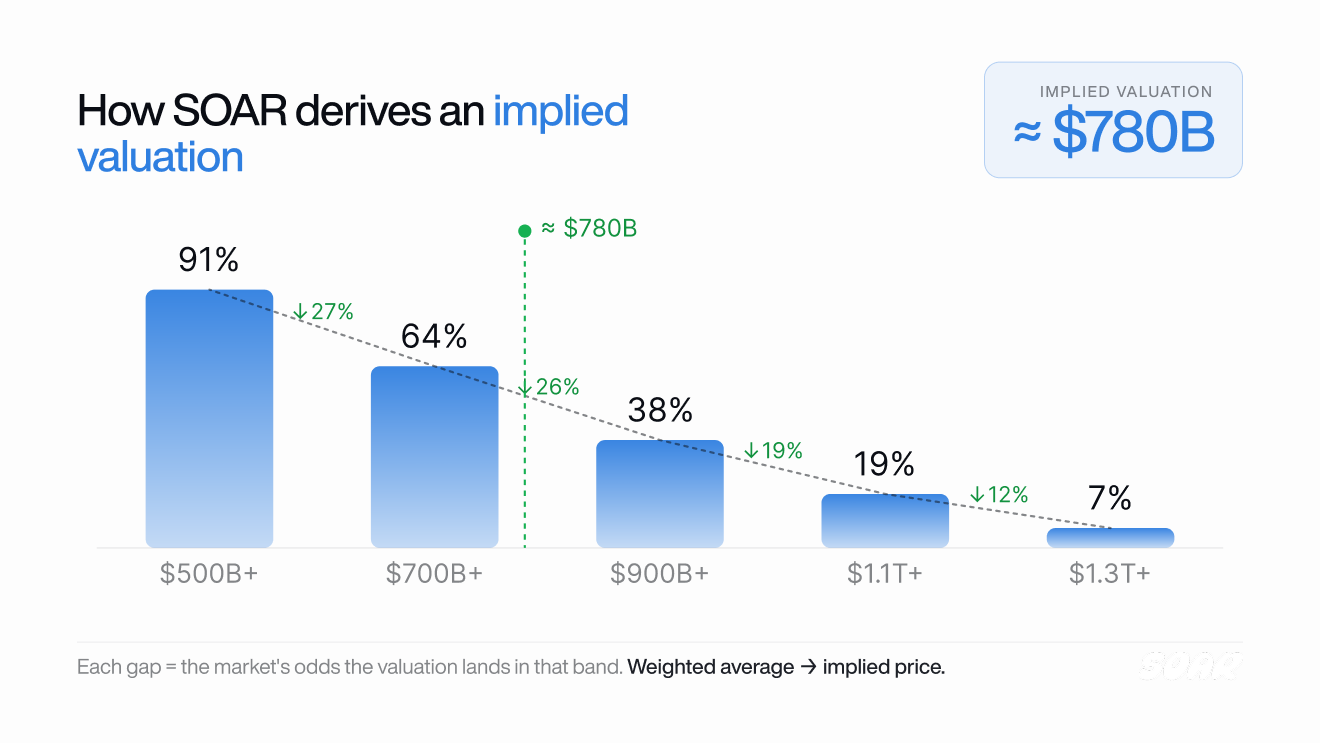

Say SOAR has five markets on Anthropic's next funding round:

Will Anthropic raise at $500B+? → 91% yes

Will Anthropic raise at $700B+? → 64% yes

Will Anthropic raise at $900B+? → 38% yes

Will Anthropic raise at $1.1T+? → 19% yes

Will Anthropic raise at $1.3T+? → 7% yes

The gap between each market is the probability the true valuation falls in that range. Aggregate those and you get a single implied valuation — what the market collectively thinks Anthropic is actually worth, updated in real time with every trade. No funding round. No investment bank. Just traders putting money behind their conviction.

The result is exposure to private companies that doesn't behave like anything else in the market. Prices move in real time, not when a company chooses to raise.

There's no accreditation requirement. There's no lock-up — positions can be entered and exited the way you'd trade any liquid market. And critically, no equity changes hands, which means no ROFR clauses, no company approval, no transfer restrictions. The synthetic is the instrument, and the instrument is open.

---

Risks of using synthetic assets

The main risks across synthetic instruments are counterparty risk, tracking error, leverage, and — for prediction markets specifically — resolution and liquidity risk.

Counterparty risk. Many synthetics depend on the other side of the trade honoring the contract. CFDs and total return swaps carry the credit risk of the broker or bank issuing them.

Tracking error. Synthetic instruments don't always perfectly replicate the underlying. ETF tracking error, oracle delays in tokenized synthetics, and basis risk in futures all create slippage between the synthetic and the real asset.

Leverage. CFDs, perpetuals, and futures are leveraged by default. According to FCA data, the majority of retail CFD traders lose money, mostly because of leverage rather than instrument failure. Most synthetic blow-ups are leverage stories.

Prediction market specific risk. Resolution risk is the big one — how the market settles, and what happens if the outcome is ambiguous. Liquidity risk matters on new markets where order books are still thin.

The honest trade-off. You can be completely right about a company and still lose if the market doesn't agree within your time horizon. Synthetic exposure is speculative even when the underlying thesis is right.

Bottom line

Synthetic assets have always existed to solve access problems. Futures emerged for commodities people couldn't physically hold. ETFs took off for indices people couldn't easily replicate. Crypto perps now move hundreds of billions a day because they solved leveraged exposure in markets that traditional brokers wouldn't touch. The pattern repeats every time finance hits a wall.

Private companies are the next wall. Ten trillion dollars in value sits behind accreditation, minimums, and lock-ups that traditional synthetics can't cross. Prediction markets — and SOAR specifically — are the first instruments built for that problem. The category is new. The mechanism is proven. The companies are the ones people already follow.

---

Disclaimer: This article is for informational and educational purposes only and does not constitute investment, legal, or tax advice. Synthetic instruments including prediction market contracts carry risk of loss, and past performance is not indicative of future results. Readers should consult a qualified financial professional and review platform-specific terms and risk disclosures before making investment or trading decisions. Valuation figures referenced may have changed since publication.