How to Invest in Startups: A Complete Guide

Key takeaways

Why has startup investing attracted so much interest?

Private companies are staying private longer than ever — the median time from founding to IPO has more than doubled since 2000, per PitchBook. That means the highest-growth phase of the world’s most valuable companies now happens entirely outside public markets. Investors have noticed.

What are the main ways to invest in private companies in 2026?

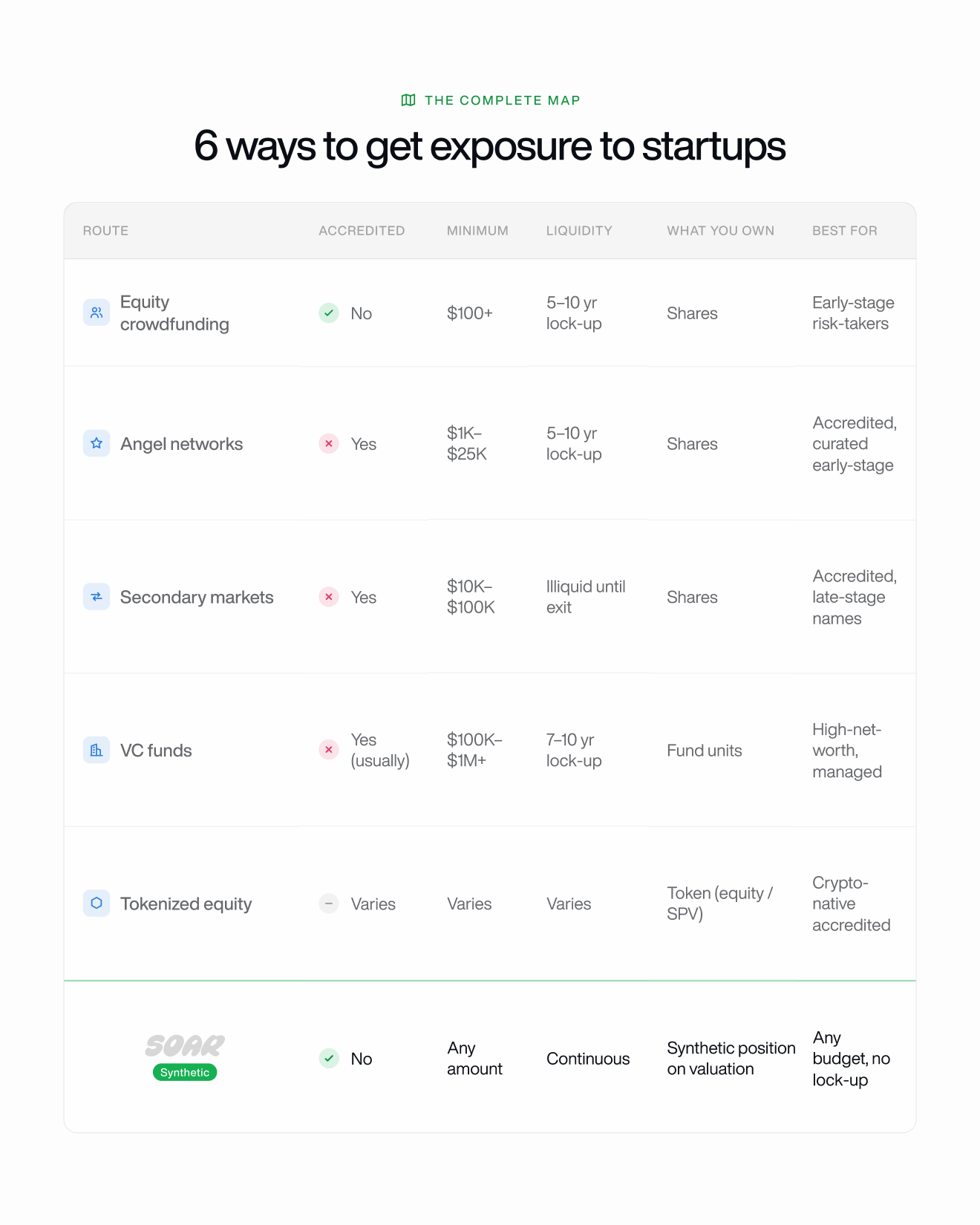

There are six main routes: equity crowdfunding (open to everyone), angel networks and startup platforms, secondary markets, VC funds, tokenized equity, and synthetic positions via platforms like SOAR. Each has different access requirements, minimums, and liquidity profiles.

Do you need to be an accredited investor to invest in startups?

Not always. Equity crowdfunding platforms like Republic and Wefunder are open to non-accredited investors under SEC Regulation CF. Synthetic positions via SOAR also require no accreditation. Secondary markets, angel networks, and VC funds typically require accredited investor status.

What is the newest way to get exposure to private companies?

Synthetic positions — financial instruments that replicate the economic exposure of an asset without requiring direct ownership — are the newest route. SOAR is a startup trading platform that applies this mechanic to private tech companies like Anthropic, SpaceX, and Stripe, with no accreditation requirement and continuous liquidity.

Table of contents

- Private company investing has never been more relevant

- Equity crowdfunding

- Angel networks and startup platforms

- Secondary markets

- VC funds

- Tokenized equity

- Synthetic positions via SOAR

- How to choose the right route for you

---

1. Private company investing has never been more relevant

Interest in startup and private company investing has surged over the last decade — and the numbers explain why. The median time from founding to IPO now exceeds 12 years, up from around 4 years in the 1990s, according to PitchBook. That shift has moved enormous value creation out of public reach.

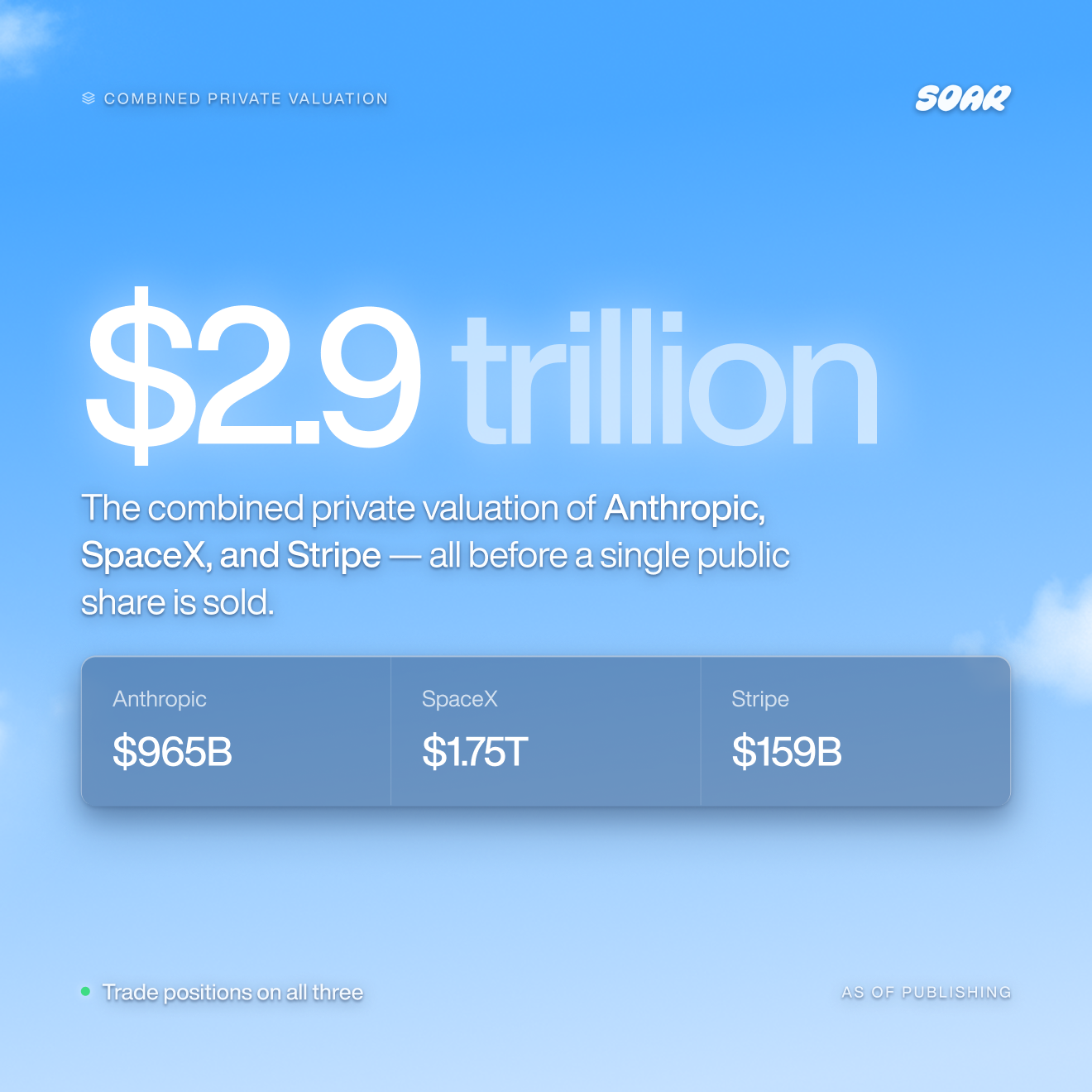

Anthropic is valued at $965 billion, SpaceX at $1.75 Trillion, and Stripe at $159 billion — all while private, all inaccessible to most investors. For context, Nvidia was worth approximately $500 million at its IPO in 1999. The extraordinary run that followed happened in public markets. Today’s equivalent companies are building that same value privately, and the question of how to access it has become one of the most searched topics in personal finance.

The growth in interest is reflected in the infrastructure that’s emerged to meet it. Equity crowdfunding platforms have raised over $2 billion cumulatively since Regulation CF passed in 2016, . Secondary market platforms like Forge Global and EquityZen have processed billions in private share transactions. And entirely new categories — tokenized equity, synthetic positions — have emerged specifically to solve the access problem that traditional structures couldn’t.

Why do companies stay private for so long now?

Companies stay private longer because private capital markets have deepened dramatically — there is more money available at later stages than ever before, removing the funding pressure that historically pushed companies toward IPO. Regulatory burdens, disclosure requirements, and the cost of being a public company are also factors. The result: companies like Stripe, SpaceX and Databricks can raise billions privately and have no urgent reason to list.

2. Equity crowdfunding

Equity crowdfunding allows both accredited and non-accredited investors to buy small equity stakes in early-stage companies through SEC-registered platforms like Republic, Wefunder, and StartEngine, under Regulation CF, which permits companies to raise up to $5 million annually from the public.

This is the most accessible route on paper. Minimums start from $100, no accreditation is needed, and the platforms are regulated and relatively straightforward to use. Republic alone has facilitated investment from over one million investors since its founding.

Equity crowdfunding platforms list early-stage startups — companies at seed or Series A stage that typically have high failure rates and long time horizons before any return. The companies most people want exposure to in 2026 — Anthropic, SpaceX, OpenAI, Stripe — don’t raise on these platforms. You’re betting on the next Anthropic, not Anthropic itself. Lock-up periods run 5–10 years, dilution from future funding rounds is common, and secondary liquidity for crowdfunded shares is essentially nonexistent.

3. Angel networks and startup platforms

Angel investing platforms like AngelList allow accredited investors to co-invest alongside experienced angels and venture capitalists in curated early-stage deals, typically through a syndicate structure where a lead investor sources and vets the deal.

The syndicate model is the key differentiator from crowdfunding. Instead of picking companies yourself, you’re investing alongside someone with deal-flow and diligence experience. AngelList has facilitated over $2.5 billion in startup investments since launch, per company disclosures. OurCrowd operates similarly with a stronger institutional co-investor base.

The catch: accreditation is typically required, minimums are higher than crowdfunding (usually $1,000–$25,000 per deal), and the fundamental risk profile is the same — early-stage companies fail at high rates.

What is an accredited investor and does it affect my options?

An accredited investor is an individual who meets SEC income thresholds ($200,000+ annually, or $300,000 jointly) or net worth requirements ($1 million+ excluding primary residence). Accreditation unlocks access to most private investment opportunities including angel networks, secondary markets, and VC funds. Non-accredited investors are limited to equity crowdfunding platforms and synthetic positions via platforms like SOAR.

4. Secondary markets

Secondary market platforms like Forge Global, EquityZen, and Hiive allow accredited investors to buy existing shares in late-stage private companies from employees and early investors seeking liquidity, with transaction prices set through a negotiated marketplace rather than a public exchange.

This is the closest traditional route to buying the companies people actually follow. SpaceX, Stripe, OpenAI, and others have traded on secondary platforms. Forge Global alone has facilitated over $15 billion in private company transactions since founding. Prices on secondary platforms are more current than formal valuation rounds and reflect real supply and demand between motivated buyers and sellers.

ccreditation is required. Minimum investments typically run $10,000–$100,000. Right of First Refusal clauses — standard in most private company shareholder agreements — mean the company or existing investors can block your transaction at the last minute by matching your offer. They are illiquid by nature: you are locked in until the company IPOs, gets acquired, or finds another buyer. And some of the most sought-after names have actively halted secondary trading; Anthropic and OpenAI have both restricted secondary market activity at various points in the last two years.

What is a Right of First Refusal and how does it affect secondary trades?

A Right of First Refusal (ROFR) is a clause in most private company shareholder agreements giving the company — and often existing investors — the right to match any secondary sale offer before the transaction can complete. In practice, it means a deal you’ve agreed to can be absorbed or blocked at the last minute, creating real uncertainty for secondary buyers and sometimes making it impossible to complete a transaction in sought-after companies.

5. VC funds

Venture capital funds, fund-of-funds, and interval funds like the ARK Venture Fund provide accredited and institutional investors with managed, diversified exposure to portfolios of private companies, with professional managers handling deal sourcing, diligence, and portfolio management.

The appeal is diversification and professional management. Instead of picking a single company, you’re buying a slice of a portfolio across dozens of bets. Some VC-adjacent structures like interval funds are more accessible than traditional LP vehicles — the ARK Venture Fund, for example, is structured as a non-traded closed-end fund with quarterly liquidity windows rather than a 10-year lockup.

The constraints are the most severe of any route here. Traditional VC fund minimums run $100,000–$1,000,000+, with 7–10 year lock-up periods standard. Accreditation or qualified purchaser status is typically required. And you surrender all control over which companies you’re invested in — the fund manager decides. This structure is built for institutional capital and high-net-worth individuals, not the retail investor trying to express a view on a specific company they follow.

6. Tokenized equity

Tokenized equity platforms like Securitize and tZERO use blockchain technology to represent ownership of private company shares, fund interests, or revenue stakes as digital tokens, enabling on-chain transfer and settlement of private market assets.

By representing securities as tokens, platforms can theoretically enable faster settlement, fractional ownership, and secondary liquidity that traditional private market structures don’t allow. Securitize has processed over $1 billion in tokenized security transactions, per company data.

In practice, the constraints remain significant. Some tokenized equity platforms still require accreditation — these are regulated securities regardless of the token wrapper. The regulatory environment is still evolving, with the SEC treating tokenized securities as equivalent to traditional private placements in most cases. Secondary markets for tokenized securities exist but remain thin; the token doesn’t automatically create liquidity if there are no willing buyers. And the specific companies most people want — Anthropic, SpaceX — are not currently available as tokenized equity. The technology is real; the accessible opportunity is still catching up.

Other variations of tokenized equity platforms may include those, such as Pre Stocks and ventuals who provide perpetual futures markets with tokens backed by SPV shares.

7. Synthetic positions via SOAR

Synthetic positions are financial instruments that replicate the economic exposure of an asset without requiring direct ownership — instead of buying a share, you take a position on an outcome, and that position gains or loses value as market consensus about that outcome shifts.

SOAR is a startup trading platform that applies this mechanic specifically to private tech companies. Rather than buying Anthropic equity through a secondary market that may block your transaction, you trade positions on specific Anthropic outcomes: will its next funding round price above $1 trillion? Will it IPO before 2028? Each market has continuous pricing driven by what traders collectively believe, updated in real time as new information emerges. The same mechanic applies across SOAR’s full roster — SpaceX, Stripe, OpenAI, and others.

The structural difference from every other route on this list is significant. No accreditation is required. There is no minimum position size. There is no lock-up — positions can be entered and exited like any liquid market. There is no Right of First Refusal, no company gatekeeper, no stale price that only updates when a company chooses to raise. The price reflects what the market thinks, right now, built from real conviction.

This isn’t equity ownership — it’s market exposure. That distinction matters for investors who want a long-term stake and ownership rights. But for anyone who wants active, liquid access to the private companies defining the next decade, synthetics via SOAR are the only route that removes every structural barrier at once.

Check out our article for deeper explanation of how synthetic positions work.

8. How to choose the right route for you

The right route depends on three things: whether you’re accredited, how long you can lock up capital, and whether you want equity ownership or market exposure.

Are you accredited?

- If no, equity crowdfunding and synthetic positions via SOAR are your two realistic options.

- If yes, all six routes are available.

How long can you lock up capital?

Every route except synthetic positions locks you in for years. If you need flexibility — or simply want to be able to exit when your thesis changes — synthetics are the only route with continuous liquidity.

Do you want equity ownership or market exposure?

Equity ownership gives you actual shares with upside and voting rights, but comes with lock-ups, ROFR risk, accreditation requirements, and illiquidity. Market exposure via synthetic positions trades the certificate for liquidity, accessibility, and real-time pricing.

Nowadays, there are many ways to get exposure to early-stage companies. Whether its through equity investments, tokenized products or synthetics, there is something for every type of market participant.

Frequently asked questions

How do I invest in startups with little money?

Equity crowdfunding platforms like Republic and Wefunder allow investments from $100 with no accreditation required. Synthetic positions via SOAR have no minimum position size. Both routes are accessible to retail investors regardless of capital size, though risk profiles and what you own differ significantly.

Can I invest in Anthropic or SpaceX as a regular investor?

Not through traditional equity routes — both companies are restricted to accredited investors and have limited or halted secondary market activity at various points. Synthetic positions via SOAR allow non-accredited investors to take positions on Anthropic and SpaceX outcomes with no minimum and continuous liquidity, without requiring equity ownership.

What is the difference between owning equity and getting exposure to a company?

Owning equity means holding actual shares with legal ownership rights, potential dividends, and upside on exit — but also lock-ups, accreditation requirements, and illiquidity. Getting exposure means your position gains or loses value based on how the company performs or how market consensus shifts, without the legal ownership wrapper. Synthetic positions provide exposure without equity.

What happens if a startup I invest in fails?

In equity routes — crowdfunding, angel networks, secondaries — a company failure typically means losing your entire investment, as most startups have no assets to return to shareholders. In synthetic positions, your loss is limited to the amount you committed to that position, and you can exit at any time before resolution if your view changes.

Is startup investing risky?

Yes — across all routes. Early-stage startups have high failure rates; the majority do not return capital to investors. Late-stage secondary investments carry less company risk but significant illiquidity and structural risk. Synthetic positions carry market risk — positions can move against you based on changing consensus. All routes require genuine risk tolerance and should represent only a portion of a diversified portfolio.