Citadel Securities alone trades nearly a quarter of all US equity volume every single day. Add Virtu, Jane Street, and the rest of the big market makers and a handful of quant firms sit on the other side of an enormous share of what America trades. They are faster than you, better capitalized than you, and execute on terms a retail trader will never touch. Direct feeds, colocation, dark pools, and the ability to work size without showing it. A Robinhood user does not get the same fills as a Citadel desk, and pretending otherwise would be dishonest.

In spite of this, nobody argues the stock market is rigged.

First, the venue itself is neutral, the exchange matches buyers and sellers, that's all. Second, the retail investor isn't playing Citadel's game in the first place. Citadel profits on tiny spreads and inefficiencies while retail investors are buying Apple to hold for a decade. The edge that prints money for Citadel is irrelevant to someone capturing ten years of a company's growth and can even improve fills for a buyer. They share the same market without ever competing for the same dollars.

That is what a healthy market looks like. A place where participants can play their edge and not have pre-determined winners and losers. This is the exact market we are building for private companies.

Where the market category went wrong

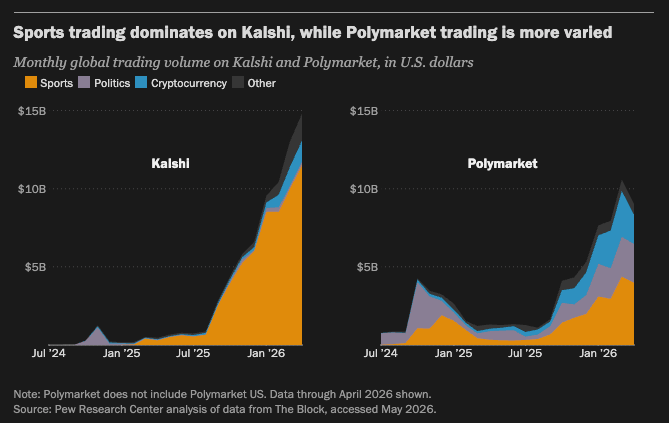

Kalshi and Polymarket have successfully made prediction markets, specifically binary outcome contracts, widely adopted by the mainstream by financializing nearly everything. You can trade sports outcomes, elections, or even a celebrity saying a word on TV. On paper this sounds awesome (it is), but there are structural inefficiencies that ultimately lead to retail participants playing for fun and losing to trading firms who are definitely not playing for fun (not so awesome).

You couldn't have missed the fight between Matt Kalish and Kalshi.

Let me introduce you to the market maker peer you’re trading sports with while mashing buttons for funsies on the @Kalshi app. We are talking nanoseconds bitch. Karl Anthony Towns over 11.5 rebounds snapped by Wall Street in microseconds bitch. Is it clocking for you?

DraftKings on one side, Kalshi on the other, arguing over whose market is fairer to the people trading on it.Kalish (confusing, I know) argues that Kalshi, by calling itself a "peer-to-peer market" with no house edge, has effectively handed the role of the house to Wall Street. Less informed participants end up matched against the most sophisticated counterparties. In the broadest sense, Matt is right. The markets that have scaled in this category are overwhelmingly sports and gambling-adjacent (roughly 80 percent of Kalshi's volume) and in those markets the more informed side wins. However, this is not unique to Kalshi. It's where the volume is, and any venue operating in that category would gravitate to the same place.

Part of his case is the mechanics. Kalish points to Kalshi exposing user identifiers in its block-quote/RFQ flow, so a market maker filling an order doesn't just see the order, they see who is behind it, and given enough reps they learn which users to stop quoting tightly because that flow is toxic (more informed than the maker pricing against it). Contrary to what Matt implies, this part is standard practice in most financial markets. Futures and equity desks quote named flow all day, and revealing who is asking is simply how request-for-quote has always worked. On its own it isn't the scandal he's making it out to be.

The core issue is not the mechanic, and it is not any one company. It's that peer-to-peer event markets sell themselves as fair fights between participants while the structure underneath funnels naive flow toward sophisticated counterparties. A venue doesn't have to be malicious for this to happen. The marketing says "trade against each other," but really you're trading against Susquehanna.

Kalshi's rebuttal to Kalish is fair too. DraftKings and the other sportsbooks limit or outright ban sharp bettors. Functionally these are the same constraint: you're either limited in how much capital you can put to work, or limited in the price you can get it filled at while keeping your edge.

Our objective is to build markets where every kind of participant can compete, where some will still lose, but where losing is never a structural certainty engineered into the venue.

Why startup markets clear the bar

The reason these markets extract from retail isn't that anyone running them is a bad actor. It's that sports, mentions, and political markets carry structural information asymmetries the venue's revenue ends up depending on (hence 80% of Kalshi’s volume being on sports). A trading firm that prices an NBA rebound total has highly sophisticated models backed by years of data alongside realtime pricing, while a typical trader is acting off an intuition. That's a significant gap in approach, and more often than not ends up funneling capital to the firm from the trader.

Private company markets don't operate in the same way, and the difference is structural. We’ve talked to every major data provider in private markets, and they all share the same sentiment. Information is extremely fragmented, backward-looking, and they're just trying to put their best guess on valuations from what is observable. Susquehanna does not get a number that the rest of us can’t see, everyone operates on the same fragmented and incomplete picture.

This fundamentally shifts who holds the edge. In sports markets, edge belongs to the firm that has faster data ingestion, and that is certainly never a retail trader. However, in a private company market the edge belongs to whoever can reason best about the trajectory of a company, and that's not something that pure infrastructure dominates. Information and insight is divided, someone who works in AI infrastructure may understand Anthropic’s trajectory better than a trading desk, or someone who understands the semiconductor supply chain may have unique insight on industry growth. The advantage shifts away from speed and access towards insights, education, and timeframes.

That is why the structure is better for the people trading in it. Not because no one loses (people will lose) but because losing is no longer the structural default for the less sophisticated side. A thoughtful participant with genuine insight can win here in a way they never could against a rebound model. Startups are the one asset class where the playing field is level enough that the stock-market standard is actually achievable, and they are among the largest pools of value on earth that have no market prices in real time. This is the most noble and logical application of the mechanisms of a market, to aggregate and price information, and it's shocking that we still live in such an opaque world when it comes to private companies.

TLDR: For most retail participants trading in competitive markets, the largest edge they can attain is trading on longer timeframes than their counterparts. In a world where 0DTE options and 5 minute markets have become a default, we’re working to enable long duration exposure to the most exciting companies on Earth.

The price of every company at the frontier of technology is currently set by six investors in a room. SOAR is the first real attempt to make that price something public markets set instead.